Love or hate student loans, they’re here to stay. Student loan trends look grim, however, as analysts say, it will only get bigger in the coming years. More students demanding college education means more student loans. It will also mean more won’t be able to pay them back, will default, or can’t discharge them.

With the changing of the guards at the White House, things are suddenly becoming promising to some extent with regards to student loans. Will there be sweeping changes or only conservative, minimal shifts from the previous administration’s policies, which were restrictive for lower-income households? Along with the impact of the pandemic, here are the crucial student loan trends to anticipate.

Student Loan Trends Table of Contents

For a long time, among all school statistics in the US, student loans are undoubtedly one of the most serious. It has ballooned 213% from the 1980s to 2018 (Student Loan Hero) and has become second only to home loans as the biggest consumer debt saddling ordinary Americans. By the third quarter of 2020, overall student loans had ballooned to over $1.7 trillion, a 4% gain versus 2019 (CNBC, 2021).

And there are various ways student loan debts aren’t just crippling people for three decades running after they graduate. In fact, they’re also taking a toll on the national economy. At present, student loan debt is larger than credit card debt, which stands at $756 billion (Experian, 2020).

Source: Education Data (2021)

On the one hand, during the campaign period, new US President Biden promised to create a program forgiving up to $10,000 of student debt in return for each year of community or national service of up to five years. On the other hand, Democrat legislators are pushing for student loan debt relief of as much as $50,000 (CNBC, 2020).

Whatever the case, these proposals have merit in light of the student loan crisis. One thing is for sure: student loans aren’t just personal problems. They’re a national problem, and these eight trends may offer some hope.

1. Forgiveness of Student Loans

Educational loan forgiveness used to be on the back burner. The two recent election campaigns changed all that, pushing it into the public limelight. And today, one of the biggest things in student loans this year is the proposal to forgive all student loans—all $1.7 trillion of it.

In the previous administration, then Education Secretary Betsy DeVos opposed loan forgiveness across the board (Fox News, 2019). The main issue is that loans, by their very nature, should be paid. Canceling all debt means leaving the creditors high and dry, with no one left to pay the cost. And it doesn’t help that it would be unfair to those who had already paid theirs.

Impact of COVID-19

The pandemic has caused an economic downturn and massive unemployment across the US, with over 14 million Americans without jobs and a record 13% unemployment rate (Pew Research, 2020). By the end of 2020, there are 45.3 million student-loan debtors with $37,691 in debt on average (Education Data, 2020).

Last March 2020, the US government has put a stay on federal student loan payment through the Coronavirus Aid, Relief, and Economic Security Act (CARES Act). The much-needed payment holiday was originally extended twice, until January 2021 (CNBC, 2020). However, only around 35 million student borrowers are qualified for the CARES Act (Education Data, 2020).

A day before President Biden’s first day in office, the COVID-19 emergency relief programs were again stretched until September 30, 2021, for federal student loans (Student Aid, 2021). For now, everything mostly depends on the Biden administration on how much student loan per borrower will the government forgive.

Key Takeaways

- The resulting economic crisis due to the pandemic has caused 14 million US workers to lose their jobs.

- The unemployment rate skyrocketed to 13%

- In 2020, the total number of student loan debtors has upsurged to 45.3 million.

- The average amount a student loan borrower owes the government is $37,691 in 2020.

2. Public Servants’ Loan Forgiveness

Public Service Loan Forgiveness, or PSLF, is a perk offered to employees of qualified government or non-profit organizations. This means that you can receive forgiveness on your remaining direct loan balance after making at least ten years (or 120, once a month) qualifying payments while working full-time for these organizations.

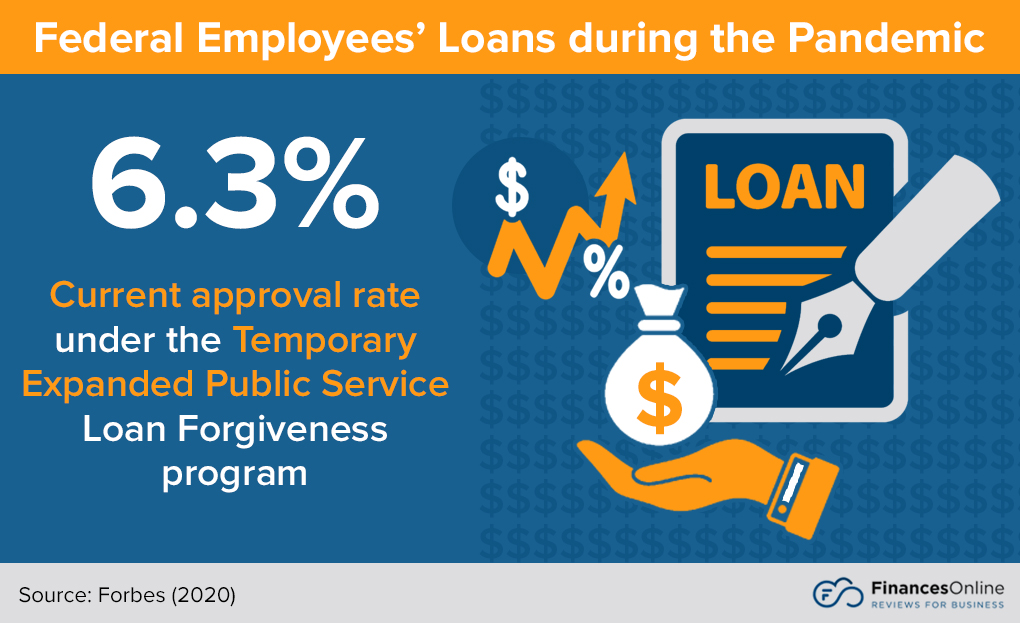

Prior to the pandemic, public service loan forgiveness was a nightmare. In December 2018, only 640 applications out of the cumulative total of 132,000 (Federal Student Aid, 2020) for public service loan forgiveness have been approved. Thanks to COVID-19, denied applications under PSLF could now appeal their case through the Temporary Expanded Public Service Loan Forgiveness (TEPSLF) program. And for 2020, out of 27,960 TEPSLF applications, 1,768 have been approved, or a 6.3% approval rate.

From PSLF to TEPSLF

During the campaign, Joe Biden agrees that the current iteration of PSLF is broken. He proposes to create a program that relieves $10,000 in student loan debt for each year of community or national service for up to 5 years (for a maximum of $50,000 debt relief) (Joe Biden, 2020). If you work for the government, an NGO, or a school, you would automatically be enrolled in this program.

At present, public servants must wait until after 120 qualifying payments or full 10 years before they become eligible for any relief. If passed, the proposed ‘‘Strengthening Loan Forgiveness for Public Servants During the COVID-19 Crisis Act” will allow student loans to be incrementally forgiven within the 10-year repayment period (US Senate, 2020). Other similar bills are being drawn in the US, mostly by Democrats (Forbes, 2020).

Key Takeaways

- Due to the pandemic, the PSLF was modified into the Temporary Expanded Public Service Loan Forgiveness (TEPSLF) program.

- The TEPSLF program has improved the loan approval rate from 0.5% to 6.3%.

- This new loan forgiveness program is just among the new initiatives that will be pushed in the new US Congress, mostly by Democrats.

3. Removal of Origination Fees on Loans

Student loans come with origination fees. These fees are the amount you pay to process your loan, usually expressed as a percentage of the total loan. Unfortunately, it’s also deducted from the loan total. For example, a loan of $10,000 with an origination fee of 4% means $400 will be deducted from your total, leaving you with $9,600. This $400—the origination fee—will go to the federal government.

Even worse, origination fees don’t stay at $400. You still pay annual interest on them, even if you haven’t really benefited from it. For a student who graduated in 2018 with an average of $28,565 in student loan debt (LendEdu, 2019), a 4% origination fee means $1,142 over four years, plus interest. And good luck if you’re looking to pursue an expensive degree, as their origination fees will be correspondingly higher.

In 2019, there were over 12 million with student loans between $10,000 to $25,000, while those who owe the government from $25,000 to $50,000 totaled 8.6 million individuals (Forbes, 2019).

Source: Forbes (2019)

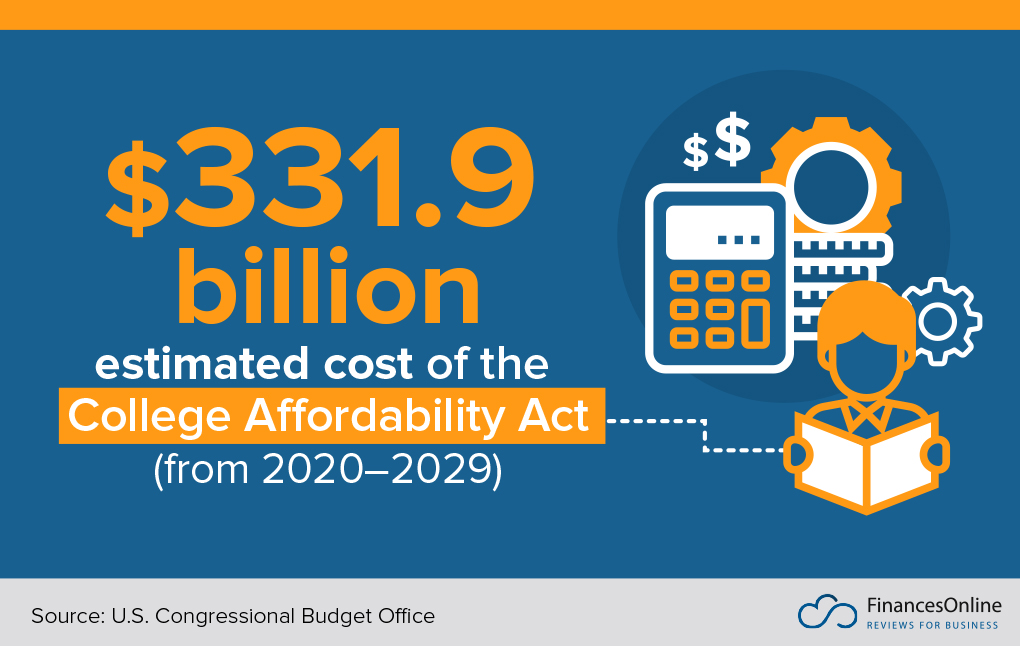

This is why House Democrats are proposing a sweeping change with the College Affordability Act (H.R. 4674) (US House of Representative, 2019). This will eliminate all hidden fees in student loans, including origination fees. While this proposed bill may cost over $400 billion over 10 years, its benefits may yet prove to outweigh its cost.

Under the Trump administration, federally subsidized and unsubsidized loans have an origination fee of 1.062%. This may yet be removed in the coming years if the House passes CAA, which has promising bipartisan support.

With the Biden White House, the origination fee for loans first disbursed from October 1, 2020 until October 1, 2021 will have a slightly lower origination fee at 1.057% (Saving for College, 2020).

Key Takeaways

- Origination fees are fees you pay to the federal government (or to a lender) to process your loan, deducted from the principal.

- Current origination fees for student loans stand at 1.057%.

- New proposals want to remove origination fees entirely, including the College Affordability Act.

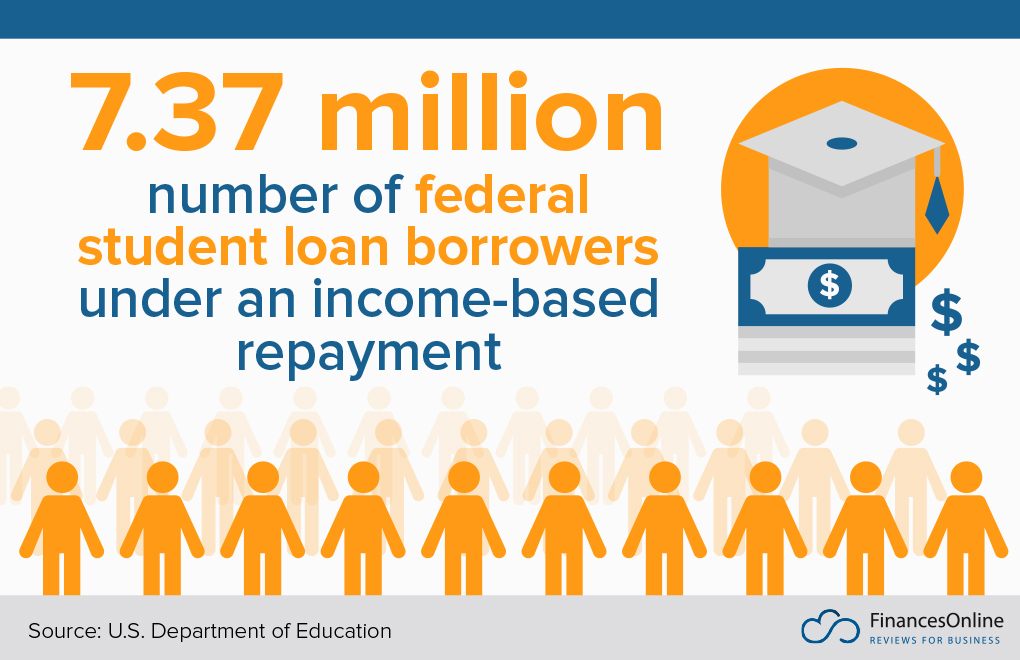

4. Income-Based Repayment

IBR is one of the two categories of student loan repayment schemes that CAA proposes (more on this below), although it’s been in existence for years. At the moment, you can avail of two kinds of income-based student loan repayment: PAYE (Pay As You Earn) and REPAYE (Revised PAYE). As mentioned above, under PAYE or REPAYE, your student loan will be forgiven after 20–25 years of qualified payments.

The operative word is, of course, “qualified.” Over the years, PAYE and REPAYE requirements have become more and more esoteric. As a result, repayments and qualifications have lagged over the last few years. Even time-tested ways on student loan repayment aren’t as effective as they once were.

This is why during his campaign, Biden expressed his view on simplifying income-based repayment. In his proposal (Joe Biden, 2020), he categorizes graduates as either making over $25,000 a year or those making less than this amount. For the former, the IBR is capped at 5% of your net or discretionary income over $25,000. After 20 years, the balance of your federal student loans will be forgiven. For those making less than $25,000, however, you would owe no payment and no interest.

Now that Biden has recently assumed the presidency, people will likely be pushing him to fulfill this campaign promise to simplify IBR in the months to come.

Key Takeaways

- Income-based repayment (IBR) is one of the few ways to pay back your student loans. This program means you can use a portion of your discretionary income every month toward your student loan debt.

- There are two major types of IBR—PAYE, and REPAYE—but their application approvals are lagging, and thus, payments.

- Simplification of IBR is in the works, notably with Biden’s proposal.

5. Student Loan Refinancing

One of the surprising student loan debt facts is that student loans are second only to mortgages (Experian, 2020) as the biggest credit category that Americans avail of. Mortgages, however, can be refinanced, but student loans can’t be. Technically you can, but only with a private lender and not with the federal government.

That is, until the CAA comes along, which is one of its provisions (US House of Representative, 2019). Being a pet bill of the Democrats, the recent take over by the part of both the executive and legislative branches to help a lot in having this bill finally passed. This bill is expected to make the federal loan program more advantageous to student loan debtors, including the option to refinance student loans at decreased rates (InsideHigherEd, 2019).

There are several great reasons to refinance your student loans, similar to why you want to refinance a mortgage. It can give you a lower interest rate, lower your monthly payment, and thus, help you pay off your student loans faster. And in this COVID-19 affected environment with high unemployment and inflation rates, this option offers numerous advantages.

That said, it may not make sense for you to refinance if you’re in a certain situation—such as bad credit, for example, though there are ways to still make a loan even with one.

Source: Experian (2020)

Key Takeaways

- Student loans are second only to mortgages as the biggest consumer debt saddling Americans.

- Mortgages can be refinanced, however, unlike student loans, allowing the debtor to pay them off much more easily with more favorable terms and interest rates.

- The College Affordability Act may change this, however, allowing debtors to refinance their student loans with federal or private lenders.

6. Review of the Higher Education Act

The CAA won’t stop with just refinancing your loan and slashing hidden fees like origination fees. It will also do other things, like making community colleges tuition-free and simplifying student loan repayment. In effect, it will review the Higher Education Act of 1965 by updating it to 21st-century educational needs and realities (US Congress, 2020).

Let’s look at the first one: making community colleges free. The CAA proposes several partnerships between the federal government and the state level to pick up the cost of college. For example, the federal government may subsidize two-thirds of the cost, with the state picking up the rest. Other ideas include providing federal funds to states that reduce or eliminate community college tuition as sort of an incentive.

Major Changes on Education Laws

The CAA also offers updates to Pell Grants (Federal Student Aid, 2021) by allowing them to cover room and board and other fees. Some provisions also include earning college credits while they’re still in high school, which can reduce their total college fees. This can work in concert with discounted fees, which, trends in higher education show, 40% of students would choose over a school with low tuition, to begin with.

In addition, the CAA also overhauls student loan repayment by consolidating them into two: the standard loan repayment scheme and an IBR. With the latter, borrowers can automatically re-certify their income after each year, which can save paperwork and time.

Interestingly, the CAA does not mention the relatively outlandish proposals offered by the 2020 presidential candidates. For example, there is no mention whatsoever of free college, which Sen. Sanders proposes, or cancellation of student debts, which both Sanders and Warren are putting forward.

Key Takeaways

- The College Affordability Act is a 21st-century overhaul of The Higher Education Act of 1965.

- Interesting provisions of the CAA include making community colleges free, where the federal government subsidizes a significant part of the tuition, and the state picks up the rest.

- It will also consolidate ways to pay back student loans into just two and empower Pell Grants to cover more than just tuition fees.

7. Loan Discharge via Bankruptcy

Most people believe that you can’t cancel or at least reduce your student loan debt by declaring bankruptcy. This is because Congress has made it so much harder to discharge your debts via bankruptcy. After all, they’re looking at a standard called “undue hardship.” This means your debts can only be discharged if you’re disabled and your disability prevents you from working. More often than not, however, it’s up to the court to decide if your situation constitutes one.

But the tables are turning. In January this year, Chief Bankruptcy Judge Cecelia Morris discharged a student loan debt (US Bankruptcy Court, 2020) amounting to $220,000 for one borrower due to Chapter 7 Bankruptcy. She says that the federal bankruptcy court in New York can and will discharge student loans if an undue hardship threshold is met—and that discharging student loans is not only possible but can also be a way to get back on your feet.

That said, bankruptcy isn’t really preferable, and will most likely be everyone’s last resort when it comes to dealing with (or discharging) student loan debts. After all, bankruptcy is a glaring red mark on your credit history.

Nonetheless, a study by the American Bankruptcy Law Journal indicates that while 40% of student loan borrowers who filed for bankruptcies have successfully discharged their loans, only 0.1% have actually tried to do so (StudentLoanHero, 2020).

Key Takeaways

- Discharging student loans due to bankruptcy is thought to be a myth because it rarely happens.

- State and the federal government only do this when the debtor has an “undue hardship,” i.e., a disability that prevents one from earning income.

- A watershed ruling by a New York Bankruptcy Judge, Cecelia Morris, however, shows that student loans can and will be discharged by bankruptcy without the borrower going through hoops to do it.

8. Free College

Sen. Sanders’ idea for his “College for All Act” entails the federal government giving each state at least $48 billion in exchange for making higher education completely free. And you’d probably think universities nationwide, including these 12 most expensive universities in America, won’t like it. It turns out it’s a mixed bag.

$48 billion is no joke, but they would have to meet a few requirements and follow a few restrictions. These include maintaining a higher standard of education, relying less on adjunct faculty, and continuing need-based financial aid. They would also have to show that they can cover each student’s college cost, especially for those in the poorest families (with annual household incomes of $25,000 or less). Restrictions include not using these funds to raise school administrator salaries. Another is that it can’t be used to fund new non-academic buildings.

While all students would benefit from this program, this proposal is especially beneficial to lower-income students (Bernie Sanders). They would also give historically Black colleges and universities (HBCUs) and minority-serving institutions (MSIs) a boost in terms of qualifying for the program. The act can allocate up to $1.3 billion annually to nonprofit universities and colleges, where at least 35% of the student population is from a low-income household. These qualifications mean about 200 higher education institutions would fit right into the program.

Free, Discounted Tuition during Pandemic

US colleges and universities are mostly shifting to fully online or hybrid (online + in-person) modes of instruction due to the pandemic. Along with this, over 25 universities are offering substantial tuition adjustments to address the uncertainties of the upcoming academic seasons (Fastweb, 2020).

- Reduced Tuition. American universities that have started to offer tuition reductions for the fall 2020 semester include Princeton University (NJ), John Hopkins University (MA), University of Pennsylvania (PA), Georgetown University (DC), and Rutgers University (NJ) (University Business, 2020).

- Tuition Freezes. Public and private US universities with tuition freezes include Duke University (NC), Bucknell University (PA), Central Michigan (MI), and College of William & Mary (VA) (CNBC, 2020; Money.com, 2020).

- Free Tuition and Scholarships. Some colleges and universities are waving tuition fees to help students continue their studies amid the pandemic. These include Southern New Hampshire University (NH), St. Norbert College (WI), Pacific Lutheran University (WA), and West Chester University (PA) (Education Dive, 2020; InsideHigherEd, 2020).

Key Takeaways

- Many colleges and universities are offering free tuition, tuition freeze, tuition reductions, etc. to help students continue their studies amid the adverse economic effects of COVID-19.

- The College for All Act proposed by Bernie Sanders will make higher education free and cancel all outstanding student loan debt.

- The proposal will call on the federal government to provide $48 billion to each state in exchange for making all school fees free for students.

Where are all those student loans heading?

Student loans are part and parcel of the American higher education landscape. With a new American President, it’s sure that college education—and by extension, student loans—will likely change. However, it remains to be seen whether these changes are minor or major, because of the inevitable, possibly lasting impact of the ongoing health outbreak.

Moreover, for a long time, it should be noted that education in America is highly cost-prohibitive. American students spend twice as much (OECD, 2019) as OECD countries do on college education. One driver of exorbitant college costs is demand even while state and federal funding are drying up. The rising costs, however, have made the advantage of a degree less important than it was 10 or 20 years ago.

This is why even the White House and Congress are waking up to the stark reality that unless this broken system is addressed, fewer and fewer Americans would have access to post-secondary education. These trends show some promise. Unless lawmakers act together for what’s good for students, student loan trends will only get worse and American education will remain a dream.

Or a nightmare, for those 45.3 million Americans mired in student loan debt.

References:

- Isler, S. (2018, May 30). Do millennials have it better or worse than generations past? Student Loan Hero.

- Hess, A. J. (2020, December 22). U.S. student debt has increased by more than 100% over the past 10 years. CNBC.

- Stolba, S. L. (2020, November 30). Consumer credit card report. Experian.

- Hess, A. J. (2020, December 17). House Democrats propose forgiving up to $50,000 in student debt—here’s what’s in the resolution. CNBC.

- Fox News. (2019, October 18). Betsy DeVos responds to Democrats’ calls to erase student debt. Fox News.

- Kochchar, R. (2020, August 26). Unemployment rose higher in three months of COVID-19 than it did in two years of the Great Recession. Pew Research Center.

- EducationData. (2021). Student loan debt statistics [2021]: Average + total debt. EducationData.

- Nova, A. (2020, December 5). Education department extends student loan payment pause for 42 million borrowers amid Covid crisis. CNBC.

- Federal Student Aid. (2021). Coronavirus and forbearance info for students, borrowers, and parents. Federal Student Aid.

- Federal Student Aid. (2020). Public service loan forgiveness data. Federal Student Aid.

- Democratic National Committee. (2020, August 3). Plan for education beyond high school. Joe Biden.

- Blumenthal, R. (2020). Strengthening loan forgiveness for public servants during the COVID-19 crisis act. US Senate.

- Minsky, A. S. (2020, May 26). Bleak new stats for public service loan forgiveness — and a potential fix. Forbes.

- LendEDU. (2019, August 8). Student loan debt by school by state report 2019. LendEDU.

- Friedman, Z. (2019, February 25). Student loan debt statistics in 2019: A $1.5 trillion crisis. Forbes.

- Education & Labor Committee. (2019, February 25). The college affordability act – Fact sheet. US House of Representatives.

- O’Connell, B. (2019, December 6). Complete list of all student loan fees. Savingforcollege.com.

- Stolba, S. L. (2020, March 9). Debt reaches new highs in 2019, but credit scores stay strong. Experian.

- Kreighbaum, A. (2019, October 16). House Democrats’ latest higher ed plan pushes free college, more generous loan repayment. Inside Higher Ed.

- Scott, R. C. (2020, December 28). H.R.4674 – 116th Congress (2019-2020): College Affordability Act. US Congress.

- Federal Student Aid. (2021). Federal Pell Grants are usually awarded only to undergraduate students. Federal Student Aid.

- US Bankruptcy Court. (2020, January 7). Memorandum decision and order granting summary judgment in favor of plaintiff and discharging debtor’s student loan under 11 U.SC. § 523(a)(8). US Bankruptcy Court.

- Isler, S. (2020, December 22). Can your debts be erased in student loan bankruptcy? Yes, here’s how. Student Loan Hero.

- Newman, S. (2020, August 18). Colleges offer free tuition, discounts due to coronavirus. Fastweb.

- Zalaznick, M. (2020, August 25). Who’s joining the list of colleges cutting tuition? University Business Magazine.

- Dickler, J. (2020, May 7). Colleges consider a tuition freeze amid pandemic. CNBC.

- Nesbitt, J. (2020, August 4). Colleges are freezing tuition and fees as classes move online. Here’s how much that actually saves students. Money.

- Schwartz, N. (2020, August 5). As an uncertain fall looms, some colleges turn to free tuition. Higher Ed Dive.

- Whitford, E. (2020, August 5). Two colleges announce tuition-free, additional time on campus for returning and new students. Inside Higher Ed.

- OECD. (2019). Education at a glance 2019: United States. OECD.

Leave a comment!