Fintech is the term that describes the group of new financial technologies designed to enhance and automate the use and delivery of financial services. It is changing how we save, borrow, and invest money by making digital financial transactions easier and simpler, without the need for a traditional bank.

Money had long been making this world go round. In recent years, however, it appears fintech is taking over to call the shots. In case you’ve been living under a rock, it’s understandable to ask: What is fintech?

Financial technology is actually all around us. When we buy something, many of us use fintech instead of cash. Many use it to do various financial transactions in ways that are far more convenient than before.

Fintech will continue to transform our society in the years to come. So let’s familiarize ourselves with this highly-disruptive class of financial innovations.

What is Fintech Table of Contents

Some bits of fintech history

Financial technology applies to any innovation that involves financial transactions, be it personal use or for business. Initiated by the birth of the credit card (the 1950s) and the ATM (1960s), fintech had since been disrupting our world.

There used to be a time when fintech only pertains to the back office operations of banks or stock trading companies. The Internet boom and the rise of mobile computing had propelled fintech to become a continuing global revolution.

Today, fintech has indeed taken an important space in today’s digital world. With an expanding family of robust technological tools for personal and commercial finance, it is poised to further grow in use and impact.

(Source: Abhishek Soni/Medium.com, 2019)

Finally, a cashless society?

The long string of fintech advancements had kicked off the powerful notion of a cashless society. Almost everyone had been talking about it for quite some time now. But signs indicate that we must still live with cash for a longer time than anticipated.

Fintech will play a crucial role in making a cashless world a reality. Given the rapid pace of how technology is changing the financial world, further fintech developments will likely bring about vast improvements to business and finance.

Before fintech reaches further milestones in the near future, it pays to know now the essentials about this awesome technology. Whether we like it or not, many of us had been using some forms of fintech without the slightest idea what it’s all about. This is why we’ve prepared this definitive introduction for you.

Fintech basics

What is fintech? Fintech is defined as innovations that involve the ever-expanding integrations between digital technology and finance. Such integrations commonly seek to enhance and automate the use and delivery of financial services to consumers and businesses.

The term is also used when talking about firms that create and provide such innovative financial products and services.

What is the purpose of fintech? Fintech uses technological tools to help consumers and companies to more efficiently manage their financial transactions. Initially confined to only desktops and laptops, fintech services are now increasingly done using smartphones.

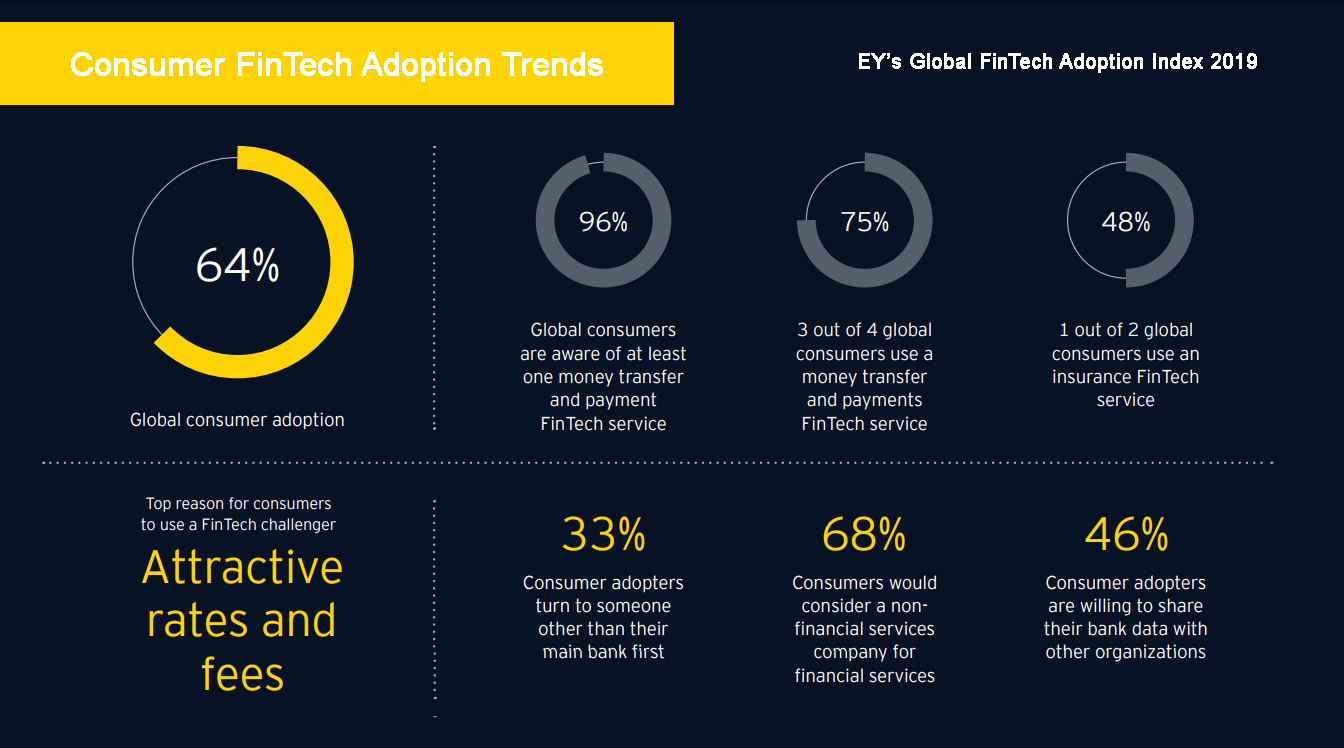

These fintech-empowered tools are changing the way many consumers track, manage and facilitate their finances. Every year, an increasing number of people across the world are using fintech. In the U.S. 64% of millennials and 59% of Gen Xers have at least one full-service banking app on their phone.

Aside from consumers, venture capitalists are contributing significantly to its global growth. For 2018 alone, Fintech firms raised an unprecedented US$39.6 billion.

From the background to center stage

From mobile payment apps to insurance and investment companies, fintech has disrupted traditional financial and banking industries. At the rate it’s growing, it is becoming a threat to the very existence of conventional, brick-and-mortar financial institutions.

At first, fintech was confined to function as back-end systems of banks. But after a myriad of innovative apps and wide applications, they’ve now gone mainstream. Today, millions of consumers and businesses are using various forms of fintech in their daily financial transactions, usually via a smartphone.

Fintech empowers approximately 2 billion people across the world with no bank accounts. It provides them easily accessible options to make them more financially viable without the help of traditional banks.

Top Countries for Fintech Services Adoption 2019

For Banking and Payments Only (accounts for 56% of worldwide total)

China: 92

China

%United States: 52

United States

%Mexico: 49

Mexico

%South Africa: 47

South Africa

%United Kingdom: 41

United Kingdom

%Source: Statista (June 2019)

Designed byDifferent types of fintech

Fintech is defined as organizations that combine innovative business models and technology to enable, enhance and disrupt financial services. Here are today’s main categories of fintechs, based on their current capabilities to make significant, real-life contributions.

Payment Gateways

Electronic payment systems had been around even before e-commerce was born. These online payment gateways have revolutionized payment, making it convenient, easy, and highly accessible for all.

The most notable contribution of payment gateways is that they allow people to send money without the need for a bank. By removing the expensive bank fees, payment gateways have given consumers considerable benefits and savings.

Aside from these advantages, fintechs are also upgrading the security aspects of online payment gateways. For instance, fintechs are developing blockchain-based systems to make electronic money transfers more secure and cost-effective, compared to banks.

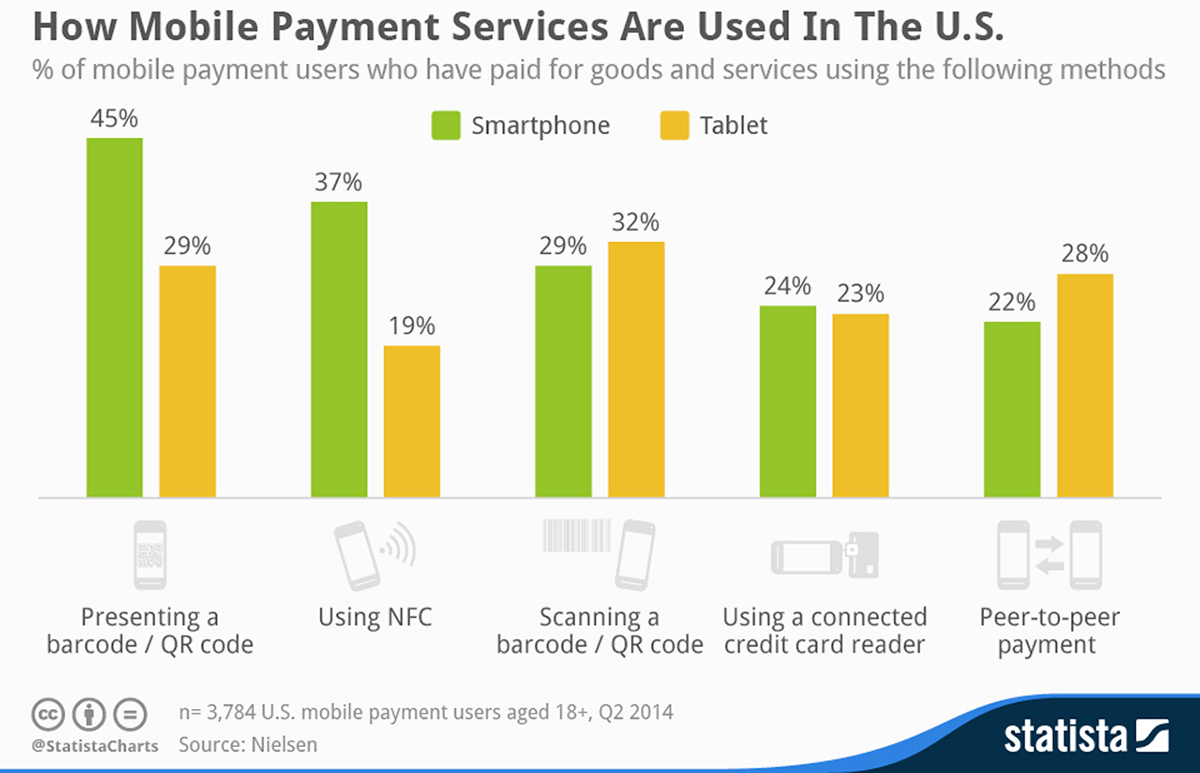

Mobile Payments

With 5.11 billion unique mobile users worldwide, it’s not surprising global mobile payment transactions will be worth over $1 trillion in 2019. By 2023, that figure is expected to exceed US$4.3 trillion.

Indeed, the global diffusion of mobile payments is nothing short of being phenomenal.

It’s no wonder fintech firms are constantly improving their products and services to better serve consumers everywhere. Advancements in mobile wallet technology, digital authentication, and NFC are spearheading these developments.

If a cashless society is something that’s still quite impossible to achieve, a physical credit card-less world is fast approaching to happen.

Have you checked out today’s best mobile payment offerings? It’s good to try out some as fintechs tend to roll out new features regularly.

Budgeting Apps

People used to take the time–often in a quiet area in their homes–to calculate their expenses and make appropriate budgets. Monitoring finances commonly involve navigating through spreadsheets and rummaging through paper receipts and checks.

Today–thanks to budgeting apps–monitoring expenses and planning budgets have become easy and more efficient. In fact, one of the most used fintech offerings to date is a mobile budgeting app.

Either for personal and business purposes, budgeting apps allow anyone to easily ad effectively closely monitor their expenses, income, and other finances. These wonderful apps have truly transformed how consumers see and perform their financial activities.

Consumer Banking

Another fintech category that’s taking the world by storm is consumer banking.

At this day and age, about 1.7 billion adults remain without a bank account or access to a mobile money provider. This is mainly because traditional banks had been operating in ways that marginalize many impoverished people.

Banks’ exorbitant fees, for instance, make it impossible for the average Joe to use their services. Fintech’s alternative consumer banking products and services are designed to address this long-standing issue. By making financial products more accessible and affordable, fintech firms provide a better alternative for consumers.

Innovative fintech banking examples abound. From mobile banks to online digital banks, fintech banks are changing banking as we know it.

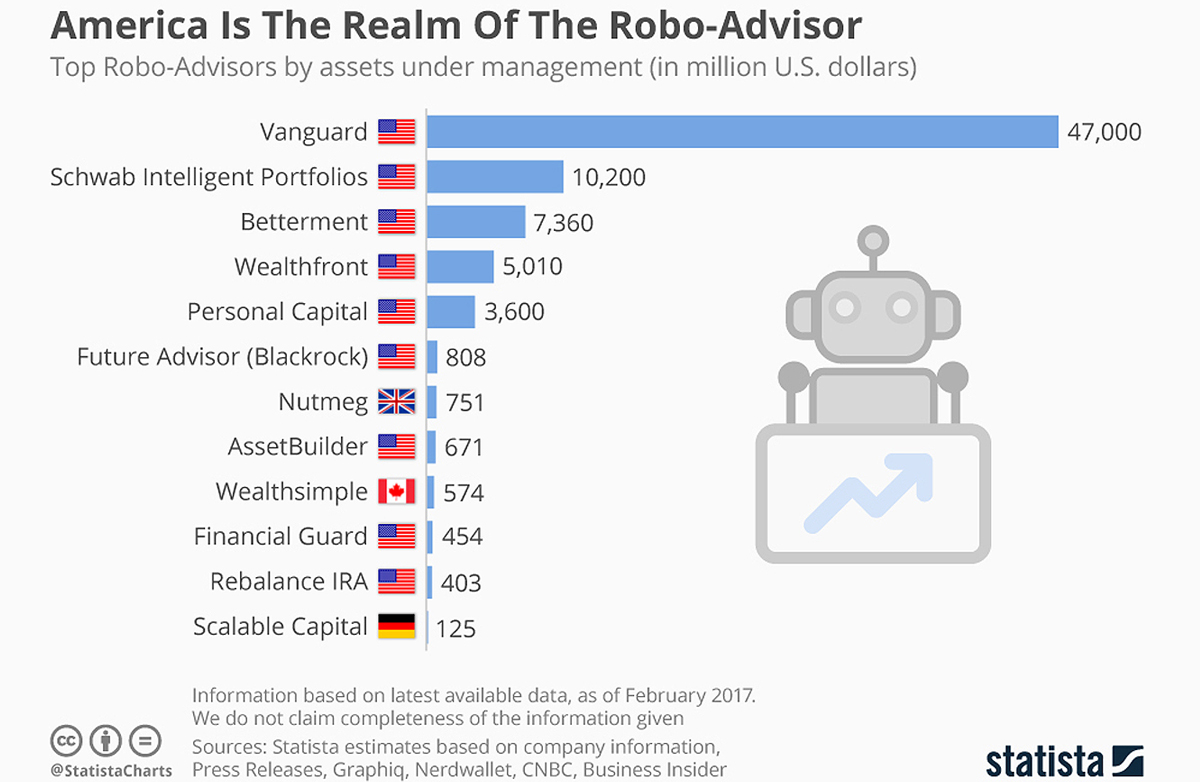

Robo-Advising and Stock-Trading Apps

In recent years, robo-advising has altered the asset management sector. This innovative fintech service uses smart algorithm technology to provide intuitive asset recommendations.

Robo-advising, in effect, portfolio management has achieved unprecedented efficiency, including lowering its costs. Financial advisers can now analyze numerous portfolio options more efficiently, 24/7, simultaneously. No wonder, an increasing number of robo-advising services continue to emerge.

Another popular and highly innovative fintech contribution is the invention of stock-trading apps.

In the past, investors must physically visit stock exchange establishments to buy and sell stocks. Today, stock trading solutions allow investors to easily trade stocks at the flick of a finger on their smartphones.

With cheaper and low-minimum stock-trading apps in the market, investing had never been easier. Thanks to these fintech innovations, making those stock-trading apps can now be done anywhere, without any budgetary constraints.

Insurance

Fintech firms have also entered the large insurance market as well, but offering better services than conventional insurers. Most insurtech firms are involved in distributing insurance.

Insurtechs are optimizing the use of innovative insurance apps to make more people insured. Like what it does in other industries, fintechs are making insurance more accessible to the underserved masses.

Firms in this category are typically collaborating with conventional insurers to automate insurance procedures and extend coverage. Insurtechs have a myriad of areas to innovate, from wearables for health insurance to mobile care insurance.

Crucial to insurance innovation is the removal of cumbersome and time-intensive processes. With fintech-provided insurance, anyone can now buy car insurance in just a few hours.

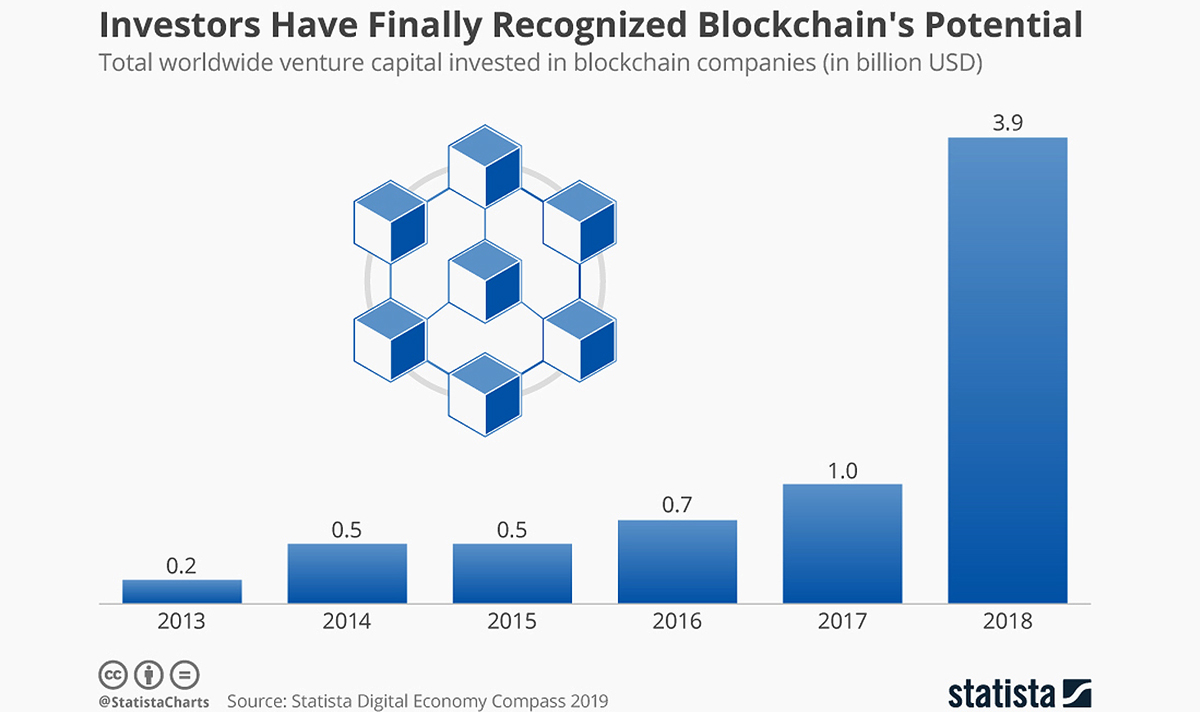

Blockchain and Cryptocurrency

Is blockchain a fintech? Yes. In fact, if there are fintech innovations that truly stand out from the rest, they’re got to be blockchains and cryptocurrencies. This is because these new technologies are offering great potential to significantly improve various industries.

Blockchain uses encryption technology to create cryptocurrencies, a promising new medium of exchange that is more secure and better than cash. In effect, blockchains offer vast possibilities to disrupt and change conventional business models.

In fact, leading organizations from various industries have already achieved significant benefits from blockchains and cryptocurrencies. These include reduced costs, faster transactions, enhanced efficiency, better traceability, improved security, and increased transparency.

A notable emerging blockchain application is that of smart contracts. These are digital, self-executing contracts that can electronically facilitate, verify, and implement agreements. Experts say that these blockchain products are likely to change how future deals will be executed.

Peer-to-peer lending/Crowdfunding

Fintech is changing how equity financing is being done as well. These innovative firms are showing the world an alternative, easier way to raise money. This approach enforces how to effectively make financial transactions outside traditional banking.

Some fintechs in this category are working to align investors with deserving startups. Others are applying virtual fundraising to facilitate new business investments.

Crowdfunding networks enable users to receive or send money online or via mobile apps. They enable businesses or individual entrepreneurs to conveniently use one location to pool funding from various sources.

It is now possible for startups to directly reach out to investors for support rather than try to secure loans from a traditional bank. You can also use donor management apps to enable better handling of P2P lending transactions.

Today’s top fintech companies

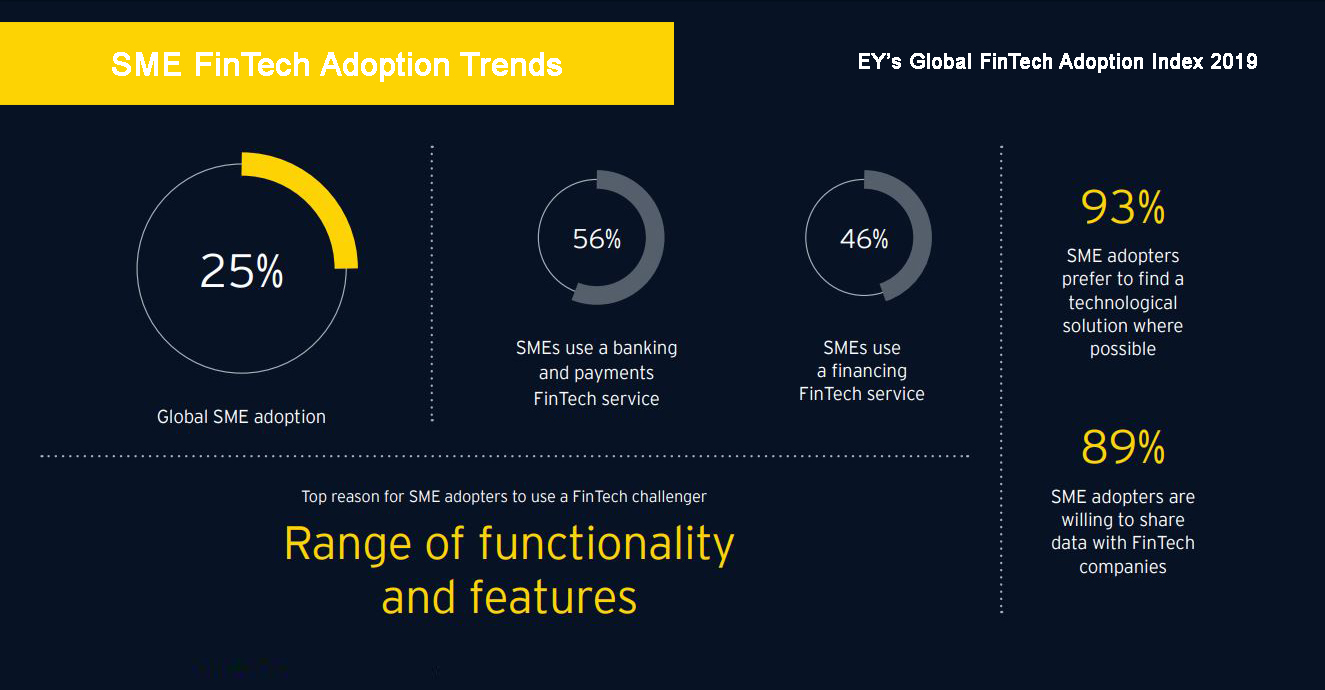

Today, 96% of consumers know of at least one alternative financial technology services they can use for making payments or transferring money. This means the entire world is aware of fintech products and services. What are examples of Fintech companies? Here are major examples of fintech firms today:

Payment gateways

- Paypal. Founded in 1998, Paypal is one of the leaders in online payment systems, especially in electronic money transfers. With over 286 million active account holders, this U.S.-based payment gateway operates in over 200 markets across the world and in over 100 currencies. Its total revenues for 2018 reached US$15.45 billion.

- Authorize.Net. One of the pioneers in digital payment systems, Authorize.Net is another “old-timer” among online payment providers, being in operations since 1996. It is now owned by Visa and focuses on providing electronic payment services to SMBs.

- Payoneer. Established in 2005, Payoneer is the mass payment gateway of choice by large global firms like Google, UpWork, and Amazon. It main offers digital payment services, online money transfer, and other popular B2B payment solutions.

Mobile Payments

- Venmo. This is a widely used mobile app, handling around $12 billion worth of transactions in 2018. A Paypal subsidiary, Venmo allows users to easily transfer funds and make payments using their smartphones at millions of establishments worldwide.

- Revel Systems. This vendor makes one of the world’s favorite retail POS systems, used in restaurants, QSRs, grocery stores, etc. Revel Systems is iPad-based and seamlessly processes mobile payments

- Apple, Inc. Made by tech giant Apple, Inc., Apple Pay is a digital wallet and mobile payment service that supports in-person contactless payment online and via iOS apps. It can accept even non-Apple Pay terminals to support mass payments.

Budgeting / Personal Finance Apps

- Intuit. The maker of the award-winning budgeting app Mint, Intuit is a Palo Alto, CA-based firm that specializes in accounting, financial, and tax preparation apps and services. Founded in 1983, this fintech’s revenues for 2017 was US$5.17 billion.

- Acorns. Based in Irvine, CA, this fintech company specializes in micro-investing services. It focuses on helping users make passive investments on exchange-traded funds

- Wally. This Dubai-based fintech makes Wally, a popular, easy-to-use personal finance app. Initially available only on iOS, the company recently launched an Android version, Wally+, to expand its user base. This app helps users make easy income vs. expense comparison as well as set and reach finance objectives.

Consumer Banking

- Green Dot. This popular banking app provides trouble-free banking for millions of people. Aside from offering dependable, affordable debit accounts, this fintech manages the biggest retail cash deposit network worldwide.

- Netspend. Founded in 1999, Netspend had served around 68 million underbanked individuals. This fintech uses special tools to provide them financial freedom, security, and convenience.

- Moven. This fintech offers a flexible smart banking platform that enables banks to lower customer acquisition costs, boost new revenue sources, and lessen customer churn rates. It uses advanced financial analytics, behavioral science, and big data to design innovative banking apps.

Robo-Advising and Stock-Trading Apps

- Vanguard. Managing US$1.3 trillion in index funds, Vanguard Group and Fidelity Investments is a market leader in robo-advising. It is among the pioneers in using blockchain technology for managing huge assets. It recently made the majority of its online trading activities free of charge.

- Robinhood. This digital upstart helped promote the zero-commission business model in the online brokerage business. Headquartered in Menlo Park, CA, Robinhood creates cash management apps for cryptocurrencies, stocks, options, and EFTs.

- Charles Schwab. The largest publicly traded e-broker, Charles Schwab services 12 million brokerage customers. This San Francisco-based stock brokerage fintech recently removed online stock trade commissions to improve its profitability.

Insurance

- Oscar Health. This New York-based fintech is the first health insurance firm designed to optimize technology to make health care simple and easy. Founded in 2012, Oscar uses transparent claims pricing systems, healthcare-focused tech systems, and telemedicine.

- Root Insurance. This unicorn tech firm offers alternative car insurance that provides drivers up to 52% savings on an insurance policy. Headquartered in Colombus, OH, Root uses technology to test driving behavior whose score determines the premium rates.

- PolicyGenius. It offers people an easy approach for comparing and buying insurance by providing complete, easy-to-understand advice. Customers are then able to better compare quotes and select which insurance suits their needs.

Blockchain and Cryptocurrency

- Blockchain. This Luxembourg-based cryptocurrency fintech makes the popular Blockchain Wallet, which is considered as one of the easiest ways to store, invest, and trade cryptocurrencies. Trusted by over 402 million wallets, it has handled over 100 million transactions involving users from 140 countries.

- Coinbase. Coinbase manages the world’s largest cryptocurrency exchange, used by more than 25 million users from 32 countries. This online marketplace allows users to sell, store, and purchase cryptocurrencies like Ethereum, Bitcoin cash, etc.

- Binance. This cryptocurrency exchange app offers one of the safest methods for cryptocurrency buying and trading across a wide range of crypto markets. It also has a mobile trading app that supports many features.

Peer-to-peer lending/Crowdfunding

- Kickstarter. Launched in 2009, this New York-based crowdfunding fintech has received over US$4.5 billion in pledges and has successfully funded over 171,000 projects to date. The company has an average success rate of 37.31% success rate.

- GoFundMe. Another leading crowdfunding firm, this for-profit crowdfunding firm has raised over US$5 billion. All its projects-which focus on helping community-based projects–are backed-up by a community of over 50 million donors across the world.

- Upstart. Founded by former Google employees, this peer-to-peer online lending firm uses non-conventional criteria to measure a person’s creditworthiness. Borrowers can loan amounts starting at $1,000 to $50,000, with a low 8.85% interest rate.

Source: BI Intelligence

Existing regulatory policies

Fintech firms continue to face costly compliance covering a myriad of financial regulations. As technology is integrated into the entire financial service ecosystem, regulatory concerns for these firms have expanded.

Most of these laws, however, are already outdated, while some are totally inapplicable to fintech. There are even cases where the problems are a function of technology. These emerging issues, basically, reflect the tech industry’s intolerance to continue disrupting finance.

The current state of regulation

While fintech firms continue to trailblaze the digital finance space, they ironically must deal with antiquated regulatory obstacles. The root cause of the problem is that fintech companies must operate in a market governed by laws created before they even existed.

In the U.S., fintechs are treated as “banks” using laws made for banks that operate during the 1970s. This, alone, perfectly captures the continued collision between the emerging technology culture and the conservative, risk-opposed finance industry.

Aside from these incongruent laws, fintechs must also deal with another challenging reality, which is to operate with the absence of related laws. A perfect example of this is the commercial diffusion of cryptocurrencies.

ICOs or initial coin offerings, used by startups to raise capital, remain unregulated. These ICOs have also become susceptible to frauds and scams.

Due to diverse fintech offerings and the discrepant industries using fintech products, it is challenging to create a single and comprehensive strategy to these legal issues. Governments mostly use existing laws, which typically caused these conflicts.

On the other hand, some are customizing laws to better regulate fintechs. In fact, some governments have created fintech sandboxes to assess the ramifications of financial technology in the various industries they operate in or affect.

Who regulates Fintech companies??

- US Federal Reserve. The Federal Reserve is the main supervisor of state-chartered banks under the American Federal Reserve System. It also supervises all bank holding companies and all fintech transactions in the U.S.

- Consumer Financial Protection Bureau. Aside from implementing federal consumer laws, the CFPB functions to protect consumers in the financial marketplace.

- Federal Deposit Insurance Corporation. Led by its FDIC Tech Lab, the FDIC is undertaking considerable reviews of existing policies to promote technology adoption within its areas of jurisdiction.

- Office of the Comptroller of the Currency. In line with its initiative to support banking innovations, the OCC now accepts applications for national bank charters from nondepository fintech firms.

- State Banking Agencies & Conference of State Bank Supervisors. At the state level, both the SBAs and CSBS are the main supervisors of nondepository financial firms like fintechs. One of its primary initiatives is to streamline licensing and harmonize the supervision of fintechs.

- Commodity Futures Trading Commission. As the main regulator of the financial derivatives market, the CFTC is also greatly involved in integrating fintech into the mainstream stock trading arena. Although not a banking regulator, the CFTC works closely with fintechs to allow better collaboration to create more innovative stock trading products and services.

What is regulatory technology?

With the ongoing antagonistic regulatory regime, fintech is taking a more proactive approach to achieve better, trouble-free diffusion. There’s now the so-called regulatory technology (or regtech) that functions to help IT-based industries like fintech to better comply with regulations.

Aside from compliance, regtechs are also working to reduce a fintech’s financial risk–usually against money laundering–by leveraging AI technology and big data. Regtech tools are also used to provide real-time monitoring of financial transactions to prevent any issues or criminal anomalies.

Regtech firms mainly use cloud computing and SaaS technologies to help companies more efficiently comply with current financial regulations. Within the fintech industry, the demand for regulatory technology is growing so fast that by 2020, regtech is predicted to become a $120 billion industry.

Different types of fintech users

Fintech companies continuously enhance financial services to be more accessible to businesses and consumers. By making financial systems easier to use and more readily available, businesses and consumers will also improve their respective affairs.

There are two main types of fintech users, namely consumer and business users. These two, there are four common, function-specific fintech user categories today. These are:

- Consumers

- B2C for small businesses

- B2B for banks

- Bank’s business clients

In the past, fintech’s growth had been slow because of its generally isolated, non-integrated applications. In recent years, however, the pace of fintech development had taken a faster rate.

Central to this accelerated growth is the creation of opportunities for all user groups to interact with each other more seamlessly. Advancements towards the decentralization of access, more accurate analytics, big data, increased information, and mobile banking will be key.

Business (B2B) Users

Before fintech’s birth and adoption, an existing and startup business owner would pay a physical bank a visit to personally conduct his or her financial transactions. Most of the banking industry’s initial involvements into fintech centered on B2C applications like payment and lending services.

Before, if a business sought to accept credit card payments, it must have a good relationship with a credit card provider to have all necessary systems installed. Now, with mobile technology advancements, such cumbersome requirements exist no more.

Beyond banks, B2B engagements are increasing further. Driven by continuing digital innovations, businesses can easily access and secure financing and other financial services.

Today’s, fintech B2B services allow companies to leverage their financial transactions to optimize their productivity and overall bottom line.

Consumer (B2C) Users

Today, fintech offers a wide array of business to client (B2C) applications. Smart cash apps like enable anyone with a smartphone to easily transfer money and conveniently manage their finances.

Same with other technological innovations, the most active fintech adopters are the younger generation. Today’s consumer-oriented fintech applications are primarily focused on millennials considering their increasing purchasing power and large segment size.

Of course, Baby Boomers and Gen Xers are not that far behind in terms of market diffusion. In fact, these two demographic groups continue to register high fintech utilization rates. This is because they have first-hand experience of the extensive benefits of fintech over traditional financial instruments.

Future trends in the fintech industry

The FinTech industry is rapidly evolving, driven by innovation, regulatory changes, and shifting consumer preferences. Here are some key trends shaping the future of FinTech:

- Rise of Digital Currencies and Blockchain Technology: Cryptocurrencies like Bitcoin and Ethereum have introduced decentralized financial models, and blockchain technology continues to disrupt industries by providing secure, transparent transactions. Central banks are also exploring Central Bank Digital Currencies (CBDCs), which could further legitimize digital currencies and reshape the global financial landscape.

- Artificial Intelligence (AI) and Machine Learning Integration: AI and machine learning are increasingly critical in personalizing financial services. From chatbots that offer customer support to algorithms that provide automated investment advice, AI is improving customer experience and operational efficiency. FinTech companies leverage these technologies to enhance credit scoring, fraud detection, and risk management.

- Growth of Neobanks: Neobanks—digital-only banks—are challenging traditional banking institutions by offering user-friendly, low-cost financial services. Without the overhead of physical branches, neo-banks can provide more attractive rates, faster service, and streamlined apps that appeal to younger, tech-savvy users.

- Open Banking and API Integrations: Open banking, where banks allow third-party providers access to their financial data via APIs (with user consent), is set to revolutionize financial services. This trend fosters the growth of new apps and services, allowing consumers more control over their financial data and making it easier to integrate different financial services.

- RegTech Innovations: Regulatory technology (RegTech) is critical in helping financial institutions comply with complex regulations efficiently. Adopting AI and automation improves compliance workflows, assisting businesses to reduce operational costs while ensuring they meet legal requirements.

Us, fintech, and the future

The entire financial world has already entered a threshold of evolution. Banks and other financial institutions are also undergoing massive changes to keep up with this transformation.

Behind all of these are the collective, powerful disruptions that fintechs bring. From how we pay and budget up to how we invest for our future, shifts will continue to occur. Fintech innovations are causing considerable tremors that will continuously change how we see and use money forever.

And with the changing of the guards–with Millennials growing in further financial capabilities–brick-and-mortar banks could likely be just a thing of the past. And who knows? Cryptocurrencies might just become that ultimate force to remove cash from our lives.

Have you already bought your first cryptocurrency yet? In case you’ve been planning to try trading bitcoins, it’s best to learn more about what bitcoin is before you make your first venture.

Key Insights

- Definition and Impact: Fintech, or financial technology, refers to innovations that integrate digital technology and finance, enhancing and automating financial services for consumers and businesses.

- Historical Context: Fintech’s roots can be traced back to the advent of credit cards in the 1950s and ATMs in the 1960s. The internet boom and mobile computing have propelled its growth, transforming it from back-office banking operations to a global revolution.

- Categories of Fintech:

- Payment Gateways: Revolutionized online payments, offering convenience and cost savings by bypassing traditional banks.

- Mobile Payments: Explosive growth in global mobile payment transactions, driven by advancements in mobile wallet technology and NFC.

- Budgeting Apps: Simplified personal and business finance management through easy-to-use mobile apps.

- Consumer Banking: Improved accessibility and affordability of banking services, addressing the needs of the underbanked.

- Robo-Advising and Stock-Trading Apps: Enhanced asset management and stock trading efficiency with smart algorithms and mobile platforms.

- Insurance: Fintech innovations are optimizing insurance processes and expanding coverage to underserved populations.

- Blockchain and Cryptocurrency: Blockchain technology and cryptocurrencies offer secure, efficient alternatives to traditional financial systems.

- Peer-to-Peer Lending/Crowdfunding: Facilitates alternative financing methods, enabling easier capital raising for startups and individual entrepreneurs.

- Regulatory Challenges: Fintech firms face outdated regulations that were designed for traditional banks. Regulatory technology (regtech) is emerging to help fintechs comply with these regulations more efficiently.

- Types of Users: Fintech serves both consumers and businesses. Consumers benefit from accessible financial tools, while businesses leverage fintech for improved financial transactions and productivity.

FAQ

- What is fintech? Fintech, short for financial technology, encompasses innovations that integrate digital technology with finance to enhance and automate financial services for consumers and businesses.

- What are the main categories of fintech? The main categories include payment gateways, mobile payments, budgeting apps, consumer banking, robo-advising and stock-trading apps, insurance, blockchain and cryptocurrency, and peer-to-peer lending/crowdfunding.

- How has fintech evolved over time? Fintech began with innovations like credit cards in the 1950s and ATMs in the 1960s. The internet boom and mobile computing transformed fintech from a back-office banking operation to a global revolution, making financial services more accessible and efficient.

- What is the impact of fintech on traditional banking? Fintech has disrupted traditional banking by providing more efficient, cost-effective, and accessible alternatives to financial services, posing a threat to the conventional brick-and-mortar banking model.

- How do fintech companies address regulatory challenges? Fintech companies use regulatory technology (regtech) to comply with existing regulations more efficiently, leveraging AI, big data, and cloud computing to reduce financial risks and ensure compliance.

- Who are the primary users of fintech? Fintech serves both consumer and business users. Consumers benefit from accessible financial tools and services, while businesses use fintech to optimize financial transactions and improve productivity.

- What role does blockchain technology play in fintech? Blockchain technology provides a secure, efficient alternative to traditional financial systems, offering benefits like reduced costs, faster transactions, enhanced security, and increased transparency. It also enables the creation and use of cryptocurrencies.

- How has mobile technology influenced fintech? Mobile technology has significantly influenced fintech by enabling mobile payments, budgeting apps, and stock-trading solutions, making financial services more accessible and convenient for users worldwide.

- What are some examples of top fintech companies? Examples include PayPal, Venmo, Intuit, Green Dot, Vanguard, Robinhood, Oscar Health, Blockchain, Coinbase, and Kickstarter, each excelling in different categories like payment gateways, mobile payments, budgeting apps, consumer banking, robo-advising, insurance, blockchain, and crowdfunding.

- What are the future trends in fintech? Future trends in fintech include further advancements in mobile payments, increased adoption of blockchain technology and cryptocurrencies, the rise of regtech, and continued disruption of traditional financial institutions by innovative fintech solutions.

this is really hard to believe such revolution is happening past quite few years but very little progress is made. for example most of the fintech companies are focusing only financial support packages rather than product based fintech application is there - ie., based on farming, local retailers, hawkers, studies and others.

interested to have a patriciate in the above and learn more on the discussion.

thanks and regards

I developed a new interest in Fintech and its regulation, I didn't have a good understanding of it. Coming across this article is a blessing as it has helped me understand what it is all about. I'm looking to do a PhD around the subject. I would be glad to receive more articles on the subject. Thank you.

Leave a comment!