There was a time when the bulk of the work of accountants consisted of bookkeeping, data entry, and number crunching. Today, the modern accountant is faced with client demands that require one to do much more than these traditional services. Much of the evolution in the accountant’s role and in the industry, in general, are aided by technology like accounting software, which eases the burden of workload so that one can focus on strategic, value-adding tasks.

The expansion of the accountant’s role is just one of the many examples of emerging trends in accounting. In this article, you can learn about the trends and market forces that point to the future of accounting. From automation and AI to data security, there are a lot of accounting software trends for 2022 that professionals in the industry need to keep track of to stay competitive in their field. Being aware of these trends will not only add to their professional competence but also inspire them to innovate for the betterment of their firm and the welfare of their clients.

Accounting Software Trends Table of Contents

Human and technological factors are driving changes that are shaking up the accounting industry today. The human aspect involves disruptions in the labor market in what pundits are calling The Great Resignation. A Microsoft report reveals that hybrid work is the next great disruption, with 41% of employees considering leaving their current employer in 2021 and 46% saying that they are likely to move because they can now work remotely. Moreover, accounting firm turnover is pegged upwards of 20% per year for most firms, which is seen to worsen because of this phenomenon (Accounting Today, 2022).

Employee Resignation and Remote Work Statistics 2021

Source: Microsoft, 2021

Designed byThere is a confluence of innovations that make up the technology component of industry changes. One interesting development is the investment in the metaverse. One of the big four accounting firms, PricewaterhouseCoopers, recently bought virtual land in Sandbox, making it the first globally recognized professional services brand to enter the metaverse. A spokesperson for Sandbox has said that the land acquisition will allow PwC to provide immersive experiences and connect with customers.

List of Accounting Software Trends

1. Decline in Accounting Software Spend

The pandemic has driven client expectations beyond traditional services to include a diverse service menu. Nowadays, they don’t just seek core accounting or bookkeeping advice. They also seek guidance on how to comply with emergency legislation, leverage government assistance, and compute leave entitlements and wage subsidies.

To address these concerns, accountants have started to veer away from traditional service models to new technologies. As a result, 58% of accountants said that prioritizing technology can give clients faster service with the help of technology. In addition, 43% believe that it means their client service and satisfaction have improved (Sage, 2020).

Be that as it may, the pandemic has affected the purchasing decisions of businesses for accounting software. In September 2020, 62% of technology buyers said they expected to spend the same for finance and accounting tools. Meanwhile, 18% said they will spend more while 15% said they will spend less. More recent accounting software trends show that 21% of businesses expected to reduce software spending on finance and accounting software in 2021. This made finance and accounting one of the top 10 areas where technology buyers planned to decrease spending during that fiscal year.

Top 10 Areas Where Tech Buyers Plan to Decrease Spending in 2021

Other hardware: 25%

Other hardware

25%Vertical industry: 22%

Vertical industry

22%Professional services : 22%

Professional services

22%Routers and switchers: 22%

Routers and switchers

22%HR: 20%

HR

20%Other IT: 18%

Other IT

18%Finance and accounting: 15%

Finance and accounting

15%Marketing: 15%

Marketing

15%Network solutions: 14%

Network solutions

14%Sales: 14%

Sales

14%Source: Statista, 2020

Designed byDecline in Accounting Software Spend Highlights

- Accountants have shifted from traditional to new technologies to support expanding client demands.

- Accountants believe that technology contributes to faster client service delivery and better customer satisfaction.

- Accounting software spend decreased during the pandemic but is seen to return to previous levels post-pandemic.

2. Accounting Software Integrated with ERP

For businesses to use accounting software is not a novel phenomenon. In fact, in 2020, the accounting software trends show that the market was already valued at $12.01 billion. It is further projected to reach $19.59 billion by 2026 (Research and Markets, 2021).

However, one of the examples of emerging trends in accounting is making the switch to an enterprise resource planning (ERP) system. Using an ERP allows organizations to combine their accounting data and financial data with other critical areas of their business, such as supply chain, order, and production management. Under an integrated system, all important information can be entered into a single application and is accessible across various channels.

Companies can reap numerous benefits by having all accounting and other important information under one umbrella that is your ERP. For one, it spares companies from having to spend on employee training under different systems and saves employees time from hunting down information scattered in various applications. Second, it improves collaboration because teams have a single source of truth. Third, information for analytics and reporting is at one’s fingertips to help leaders make decisions (SelectHub, 2021). However, with all its benefits, it still has its shortcomings. For instance, businesses should consider the hidden licensing costs of ERP accounting software.

Accounting Software and ERP Integration Highlights

- The market for accounting software is expected to grow in the next five years.

- While companies are already using accounting software, a growing trend is to integrate such software with their ERP.

- Accounting software integrated within an ERP saves companies time and money and helps them make data-driven decisions more quickly.

Most Popular Accounting Software

- Sage Intacct. Sage Intacct offers accounting solutions such as cash management, accounts payables and receivables, and spend management. Our Sage Intacct review provides a deeper look into the software.

- Xero. Xero makes it easy for users to track and edit transactions, monitor billing and invoicing, and even process payroll. Learn more about the software through our Xero review.

- FreeAgent. FreeAgent lets you send and track invoices, manage expenses, and use a built-in stopwatch to keep time records. Check out our full FreeAgent review to learn more.

- Gusto. Gusto comes with capabilities for automated payroll management to ensure the elimination of human errors. Find out more about the software through our Gusto review.

- Sage Business Cloud Accounting. Sage Business Cloud Accounting combines accounting, expense management, and compliance management into one platform. Read our Sage Business Cloud Accounting review to learn more.

3. AI for Accounting

Accountants and CIOs agree that artificial intelligence software is one of the emerging technologies that will shape the future of the industry. In a survey, 20% of accountants say that they are currently investing in and adopting AI technology. Another 20% said that they plan to adopt AI technology within the next 12 months (Sage, 2020). On the other hand, 47% of CIOs believe that the COVID-19 pandemic has led to the acceleration of digital transformation and adoption of emerging technology, such as artificial intelligence, machine learning, blockchain and automation (Harvey Nash/KPMG, 2020).

This early, there are already AI implementations that show that is not a technology reserved for the distant future. Twenty-four percent of small-scale emerging technology implementations are related to artificial intelligence or machine learning. Five percent of these projects are done on a large scale. The pandemic has even served to hasten AI adoption. Data shows an 11% increase in usage of AI and machine learning technologies between the pre-COVID phase of 2020 and the onset of the pandemic in the same year (Harvey Nash/KPMG, 2020).

Because AI primarily feeds on data, it is critical that businesses extract quality data. This will enable organizations to have accurate business intelligence that will give them a competitive edge. Organizations need to have the right applications, cloud solutions, analytics, and business processes in place. They should take cues from digital leaders who are four times more likely than others to make the most out of their data effectively (Harvey Nash/KPMG, 2020).

AI Adoption Among Accountants 2020

Source: Sage, 2020

Designed byAI for Accounting Highlights

- Accountants and CIOs are one in saying that AI will impact the accounting industry.

- Organizations already have AI implementations in place, although this is less than a third and are focused on small-scale projects.

- For AI implementations to be effective, quality data should be extracted to support business intelligence and decision-making.

4. More Emphasis on Data Security

Accountants often handle sensitive client information related to their finances, payroll, and taxes. As such, the occurrence of data breaches is a huge blow to their credibility and reputation and even opens them up to lawsuits. What’s alarming is that the pandemic has not slowed down cyberattacks by malicious actors. Data shows that 41% of CIOs experienced cybersecurity incidents from spear phishing and malware attacks, on top of facing cybercrime challenges before the COVID-19 health crisis. The types of cyberattacks that have increased as a result of the pandemic are spear-phishing (83%), malware (62%), and denial-of-service attacks (21%) (Harvey Nash/KPMG, 2020).

The prevalence of these events have led software consumers to be even more mindful of security issues. Top leaders are taking note of these concerns. In a survey, 47% of CIOs said that security and privacy is one of their top three most important technology investments (Harvey Nash/KPMG, 2020).

The challenge for today’s accountants and accounting firms is to be effective data collectors and handlers. To do this, they should observe security best practices, such as proper access and protocols, physical security protocols, and backup and encryption. These efforts should be complemented with security training for employees and a contingency plan in case a data breach does occur (HostReview, 2016).

Data Security Highlights

- The pandemic has not deterred cybercriminals from launching malicious attacks, which leaves financial data handled by accountants at risk.

- Software buyers and business leaders have become more mindful of security features due to the prevalence of data breaches.

- Accountants can employ good data collection and handling by implementing security best practices.

5. Utilizing Accounting Data for Insights

Investing in a robust data infrastructure opens up the possibilities for companies to implement advanced technologies. One of these is data visualization and analytics, which is crucial for sound decision-making. The good news is that organizations are inclined to harness such technologies in the workplace. Around 39.7% of finance professionals say that they are planning to implement or are currently implementing data analytics and visualization technologies. Meanwhile, 10.1% said that they already implemented such technologies (Deloitte, 2020).

The use of advanced technologies has altered the kind of services that accountants do for clients, too. For instance, 53.4% of finance and accounting professionals said that the type of work in finance has changed from “somewhat less transactional processing” to “somewhat more analytical” processing in the last 18 months. Survey respondents felt that this shift will be sustained over the next few years. In addition, 45.8% of finance and accounting professionals say that the work will be significantly more analytical in the next five years, while 45.8% also said that it will be somewhat more analytical with room for improvement (Deloitte, 2020).

With the shift from transactional to analytical processing, accountants will need to update their skill sets as well. When asked what important core skills and capabilities their team members should improve on, 61.7% of finance and accounting professionals cited critical thinking and problem-solving skills. Strong technology skills came second at 40.4% while data analytics ranked fourth at 27.3% (Deloitte, 2020).

Accounting Data for Insights Highlights

- A significant number of companies are investing in data analytics and visualization technologies.

- The work of accounting and finance professionals will shift from transaction to analytical processing.

- Critical thinking and problem-solving skills are needed for accountants to respond to the shift in the type of work they need to do.

6. Accountants as Partners of Businesses

Crunching numbers is traditionally the main function of accountants. However, as client needs change over the course of the pandemic, there came the realization that accountants can do so much more.

In a recent survey, 51% of accountants believe that those joining the profession today should be equipped with business advisory skills, such as cash flow and growth modeling. The survey also found that technology skills ranked as the most important capability for accountants to have in the next five or 10 years, at 51%. However, strategic thinking placed a close second at 43%. Other highly-ranked skills were communication skills (40%), customer service skills (30%), and deep knowledge of growing a business (29%) (Sage, 2020).

These skills will come in handy as accountants take on an advisory role instead of merely guiding clients for compliance-related functions. The trend is for accountants to deliver value to clients. In fact, 79% of accountants in the US say that client expectations have evolved to include business and finance consultancy (Sage, 2020). They can achieve this by knowing their client’s revenue streams and business models so they could dispense sound financial advice. They must analyze internal and external data about customers, markets, distribution channels, and competitors so they can help businesses formulate their strategies and make decisions (Management Accounting, 1991).

The pandemic even saw the growth of accountants as trusted advisors. In a survey, 48% of small businesses in the US say that they found the advice they have been getting from an accountant about COVID-related government relief programs as important (Onpay, 2020). This shift in job roles should ease fears that accountants will lose their jobs and should take steps to protect themselves from job automation.

Source: Onpay, 2020

Accountants as Partners of Businesses Highlights

- Accountants are expected to do more than their traditional functions such as analyzing numbers and bookkeeping.

- Skills related to business advisory, technology, and strategic thinking are deemed important skills for modern accountants to have.

- Having such skills will position them to be advisors to businesses, which helps organizations grow their business.

7. Accounting Automation as the New Standard

Many finance-related activities can be automated. A study shows that 77% of general accounting operations can be fully automated while 12% can be highly automated and 12% can be somewhat automated. These activities include complex journal entries, account reconciliations, fixed-asset account maintenance, and calculating and applying allocations. (McKinsey, 2018.). Moreover, 28.2% of finance and accounting professionals from the financial and business services sector are more likely to say that their accounting processes are mostly automated. Experts observed that firms with a high number of transactions and are mostly client-facing like banks and utility companies tend to automate their processes (Deloitte, 2020).

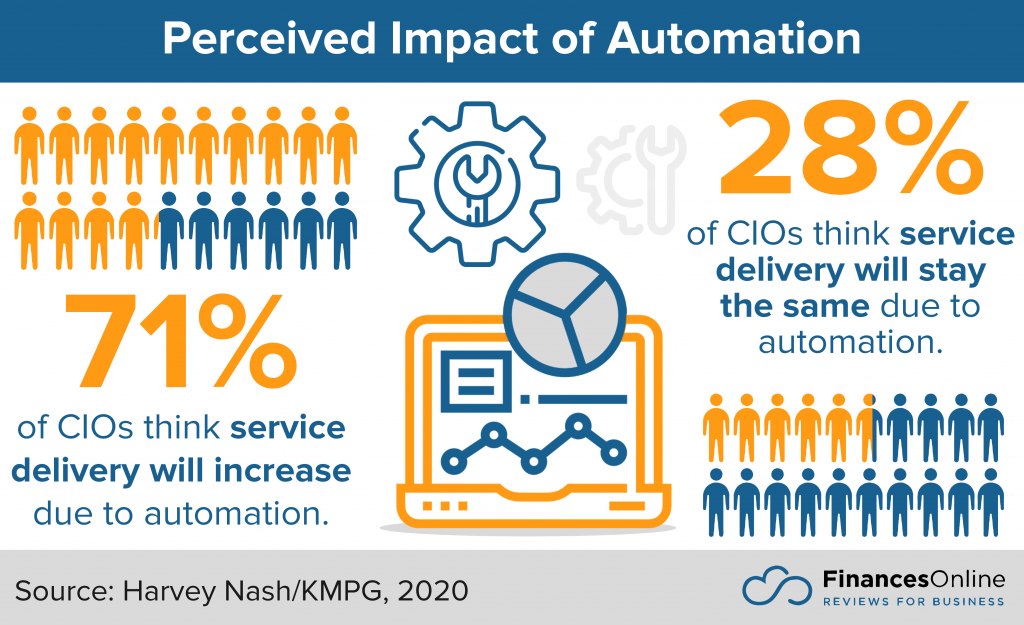

Recognizing its benefits, business leaders and finance professionals are finding ways to incorporate automation into their operations. For instance, 71% of CIOs expect their service delivery model to increase on account of automation activities (Harvey Nash/KPMG, 2020). On the other hand, 21% of finance professionals said that they are exploring automation to free up time to focus on being strategy partners and value managers (AICPA, 2020).

However, organizations aspiring to have fully automated processes still have a long way to go to complete the journey. Data shows that 42.9% of finance professionals say that their processes are still considerably manual while only 22.4% said it is largely automated. This is because organizations are currently opting to implement foundational tools like cloud-based accounting solutions rather than automation tools. As a result, there are different opinions as to when the impact of automation will be significantly felt in the workplace. Around one-third (28.3%) of finance and accounting professionals quoted a time frame of three to five years. Meanwhile, another third (27.9%) think that the impact can be felt now (Deloitte, 2020).

Accounting Automation Highlights

- A significant amount of accounting activities can be automated, especially for companies that are client-facing and have high transaction volumes.

- Business leaders and finance professionals expect automation to be part of their operations.

- Close to 50% of processes are still manual and less than a third are largely automated.

8. Demand for Transparent Reporting

Financial reporting is the most common way for the public and investors to know how well a company is performing. Having high-quality financial statements that promote transparency grows investor confidence and allows them to assess a company’s exposure to risk. The pandemic further underscored the need for companies to provide trustworthy financial information. With transparent financial reporting, firms can communicate where they stand in terms of liquidity, business continuity, and how the pandemic has impacted their business overall.

Today, there is growing pressure from various stakeholders to also report beyond the traditional financial numbers. Investors are also now more interested in sustainability, employee diversity, and other environmental, social, and governance (ESG) criteria. On average, 91% of global investors expect their firm to increase prioritization of environmental, social and governance (ESG) as an investment criterion as they recover from the pandemic. Moreover, 98% of investors in the US are considering ESG in their investment process (Edelman, 2020).

In creating more transparent reporting, it is important to have the commitment of the board of directors to creating sustainable value. It also helps to strategize and pick the appropriate reporting standards and ensure that systems are in place that makes it easy to gather financial and non-financial data. Part of this is investing in the right financial reporting software. Providing the data in flexible and engaging digital formats for third parties is likewise a key component of this emerging trend (PwC, 2021).

Transparent Accounting Reports Highlights

- Transparent accounting reporting strengthens investor confidence in a company, especially in crisis situations like the pandemic.

- Investors are now looking into environmental, social, and governance from companies aside from traditional financial reports.

- Creating transparent reporting requires board-level engagement, choosing the right reporting strategy, and making this information accessible.

9. Keeping Accounting In-House for SMBs

For businesses that are just starting out, they may be faced with the dilemma of keeping accounting in-house or outsourcing it. There are pros and cons to each side and deciding which accounting service type to pick will depend on various factors.

Data reveals that 62% of small businesses in the US have in-house accounting employees. Small business owners and managers say that there are numerous primary benefits to keeping accounting functions in-house. The top three benefits given were knowledge of business practices, flexibility with project staffing, meeting company-specific needs, all of which were cited by 21% of survey respondents. Other benefits given were easier communication (20%) and direct supervision over the accounting team (17%) (Clutch, 2021).

As small businesses grow, however, they tend to outsource their accounting activities. Statistics show that 30% of small businesses use an external accountant (Onpay, 2019). Some factors that influence the decision of small businesses to outsource accounting services include business size and the length of its existence in the market. For instance, 49% of small businesses that had the same owner or manager for five years or more have in-house accountants.

In contrast, 73% of small businesses with in-house accountants have been in business for less than one year (Clutch, 2021). Moreover, businesses with 50 or fewer employees are less likely to outsource compared to businesses with over 50 employees (Clutch, 2019). Small businesses seek the help of outsourced accountants mainly to seek their expertise on complicated issues and guidance on how to meet compliance requirements (Clutch, 2021). With widespread employee layoffs and furloughs due to the pandemic, saving on employment costs is a factor too, with 15% of small businesses saying that they have cut costs on accounting or bookkeeping services (Onpay, 2020).

Benefits of In-House Accounting According to SMBs 2021

Knowledge of business practices: 21%

Knowledge of business practices

21%Flexibility when staffing for projects: 21%

Flexibility when staffing for projects

21%Meeting company-specific needs: 21%

Meeting company-specific needs

21%Easier communication: 20%

Easier communication

20%Direct supervision of accounting team: 17%

Direct supervision of accounting team

17%Source: Clutch, 2021

Designed byIn-House Accounting Highlights

- Most small businesses keep their accounting in-house for staffing flexibility, knowledge of business practices, and fulfilling company-specific needs.

- Small businesses that have been around for one year or more and have more than 50 employees are more likely to outsource accounting functions.

- Outsourcing accounting is resorted to when small businesses need to cut costs, which was more pronounced during the pandemic.

10. Accounting Standards and Regulatory Updates

After a year or so of lockdowns and other pandemic-related restrictions, businesses worked on reopening or operating at full capacity in 2021. The US government has come to their aid by offering stimulus packages. This, in turn caused many companies to rethink the way they handle their finances. As such, accountants are working on the double to keep up with changes in payroll and taxation.

In 2020, the Coronavirus Aid, Relief, and Economic Security (CARES) Act was enacted, which gave economic aid to American small businesses and industries. In 2021, the Coronavirus Response and Consolidated Appropriations Act was signed into law, which continued most of the programs under the CARES Act with some modifications. Part of the economic aid under these laws is an employee retention credit. This gives small businesses up to $28,000 of credit per employee until 2021 to offset payroll tax liabilities. They can also avail of a tax credit of 50% of wages up to $10,000 per employee capped at $5,000 per employee. This is on top of 100% tax credit for companies that provide paid sick leave and family leave to employees (US Department of Treasury, n.d.).

For 2021, there have been proposed changes by the Financial Accounting Standards Board to the US GAAP financial reporting taxonomy. These include additional elements around leases, reorganizations, debt securities, asset acquisitions, credit losses, variable interest entities, and banking regulation disclosures. The rise in remote work will also have tax implications that accountants should take note of. For example, tax compliance can be more challenging if the employee’s home office is located outside the employer’s place of business (CPA Practice Advisor, 2021).

Source: AGA, 2021

Standards and Regulatory Updates Highlights

- COVID-19 stimulus packages will impact the way businesses report on payroll and taxation.

- Accountants should keep abreast of proposed changes to accounting standards like GAAP.

What Are the Challenges of Adopting New Accounting Software?

Adopting new accounting software can significantly improve a business’s financial management but also presents several challenges. Here are some common hurdles companies face during this transition:

- Data Migration: Transferring data from old systems to new software can be complex and time-consuming. Ensuring data accuracy and integrity during migration is crucial to avoid financial discrepancies.

- Employee Resistance: Change can be met with resistance from employees accustomed to existing processes. Training and communication are vital to help staff adapt to the new system and understand its benefits.

- Cost of Implementation: While modern accounting software can offer long-term savings, the initial implementation costs, including software purchase, training, and system integration, can be a significant barrier for many businesses.

- Integration with Existing Systems: New accounting software must often integrate seamlessly with other business applications (such as CRM or ERP systems). Compatibility issues can complicate this process, leading to operational disruptions.

- Learning Curve: Employees may need time to learn the new software. A steep learning curve can slow down productivity and affect financial reporting during the transition period.

- Customization Needs: Some businesses may require specific features or workflows that the new software doesn’t support out of the box. Customization can be costly and time-intensive.

- Vendor Reliability: Choosing the right software vendor is critical. Companies must assess the vendor’s reputation, support options, and long-term viability to ensure they make a sound investment.

- Ongoing Support and Maintenance: After the software is implemented, businesses may still face challenges related to updates, maintenance, and troubleshooting. Reliable ongoing support is essential for smooth operation.

- Security Concerns: Transitioning to new software raises concerns about data security. It is vital to ensure that the new system complies with relevant regulations and has robust security measures in place.

Accounting in a New Era

More fresh opportunities and challenges are waiting for accountants in 2022 and beyond. Increasing demands on their job brought about by higher client expectations, new laws, and revised accounting standards will require accountants and firms to update their knowledge and retool their skill sets. Meanwhile, promising new technologies like automation, artificial intelligence, and ERP integration can leave repetitive and transactional processes to machines so accountants could focus on delivering value to clients.

Accounting in a new era is not expected to be smooth-sailing for everyone involved. Optimizing technology despite reduced accounting software spend and cost-cutting measures, which result in talent outsourcing will continue to pose difficulties for accountants and firms. As such, it is imperative for them to maximize the potential of their accounting software.

Key Insights

- Decline in Accounting Software Spend

- Accountants are shifting from traditional methods to new technologies to meet expanding client demands.

- Technology prioritization contributes to faster client service delivery and improved customer satisfaction.

- Accounting software spending decreased during the pandemic but is expected to return to previous levels post-pandemic.

- Accounting Software Integrated with ERP

- The market for accounting software is projected to grow significantly in the coming years.

- Integrating accounting software with ERP systems allows for better data management and decision-making.

- ERP integration saves time and money and improves collaboration within organizations.

- AI for Accounting

- AI technology is increasingly being adopted in the accounting industry.

- Quality data is essential for effective AI implementations, which support business intelligence and decision-making.

- AI adoption has accelerated due to the pandemic, with small-scale projects being the most common.

- More Emphasis on Data Security

- Cybersecurity incidents have increased during the pandemic, posing risks to sensitive financial data.

- Security and privacy are top technology investment priorities for business leaders.

- Implementing security best practices and employee training are crucial for data protection.

- Utilizing Accounting Data for Insights

- Companies are investing in data analytics and visualization technologies to enhance decision-making.

- The role of accountants is shifting from transactional to analytical processing.

- Critical thinking and problem-solving skills are essential for accountants to adapt to this shift.

- Accountants as Partners of Businesses

- Modern accountants are expected to provide business advisory services beyond traditional accounting functions.

- Skills in technology, strategic thinking, and business growth are increasingly important.

- Accountants are becoming trusted advisors, helping businesses navigate financial and strategic challenges.

- Accounting Automation as the New Standard

- A significant portion of accounting activities can be automated, particularly in high-transaction, client-facing firms.

- Automation is expected to enhance service delivery and free up time for strategic activities.

- Despite the potential, many accounting processes remain manual, and widespread automation is still in progress.

- Demand for Transparent Reporting

- Transparent financial reporting enhances investor confidence, especially during crises like the pandemic.

- Investors are increasingly interested in ESG (Environmental, Social, and Governance) criteria.

- Effective transparent reporting requires board-level commitment and the right technological tools.

- Keeping Accounting In-House for SMBs

- Many small businesses prefer in-house accounting for better control and understanding of business practices.

- Outsourcing is more common in larger or more established small businesses.

- The pandemic has influenced cost-cutting measures, including outsourcing accounting services.

- Accounting Standards and Regulatory Updates

- COVID-19 stimulus packages have impacted payroll and taxation reporting requirements.

- Accountants must stay informed about changes to accounting standards like GAAP.

- Remote work trends will have ongoing tax compliance implications.

FAQ

- What are the emerging trends in accounting software? Emerging trends include the integration of accounting software with ERP systems, the adoption of AI technologies, increased emphasis on data security, and the use of accounting data for insights.

- How has the pandemic affected accounting software spending? During the pandemic, accounting software spending decreased, but it is expected to return to previous levels as businesses recover.

- What benefits do ERP systems provide when integrated with accounting software? ERP systems streamline data management, enhance collaboration, save time and money, and support data-driven decision-making.

- Why is data security a top priority for accountants? Accountants handle sensitive financial data, and the increase in cyberattacks during the pandemic has highlighted the need for robust data security measures.

- How is AI being used in the accounting industry? AI is being used for automation, improving business intelligence, and supporting decision-making processes, with a focus on quality data extraction.

- What skills are essential for modern accountants? Critical thinking, problem-solving, technology skills, and business advisory capabilities are crucial for modern accountants to meet evolving client expectations.

- What is the role of automation in accounting? Automation helps streamline repetitive tasks, allowing accountants to focus on strategic activities and improving overall service delivery.

- Why is transparent financial reporting important? Transparent reporting builds investor confidence, provides clarity on a company’s financial health, and meets growing demands for ESG criteria.

- Should small businesses keep accounting in-house or outsource it? The decision depends on factors like business size, duration, and specific needs. In-house accounting offers better control, while outsourcing can provide cost savings and expertise.

- What regulatory changes should accountants be aware of? Accountants should stay updated on changes related to COVID-19 stimulus packages, GAAP updates, and tax implications of remote work.

References:

- Association of International Certified Professional Accountants. (2020). Agile Finance Reimagined. Reimagining finance for the new normal. CPMG.

- Bryant, K. (2020, September 9). The Practice of Now 2020: The essential report for accountants. Sage.

- Chalmers, J. and Picard, N. (2021, January 18). Learning to love transparency. PwC.

- Deb, A. (2016, September 15). 6 Practical Tips To Keep Your Accounting Firm’s Data Secure. HostReview.

- Deloitte. (2020). From Mirage to Reality: Bringing Finance into Focus in a Digital World. Deloitte.

- Edelman. (2020). Special Report: Institutional Investors: U.S. Results. Edelman.

- Girsch-Bock, M. (2021, August 12). Top 5 Accounting Trends for 2021 and Beyond. CPA Practice Advisor.

- Harvey Nash / KPMG. (2020). Harvey Nash / KPMG CIO Survey 2020: Everything changed. Or did it?. Harvey Nash / KPMG.

- McCabe, S. (2022, January 5). Firms face the Great Resignation. Accounting Today.

- Oliver, L. (June 1991). Accountants as Business Partners. Management Accounting.

- O’Shaughnessy, K. (2021, June 24). 8 Reasons Why ERP is Important. SelectHub.

- Plaschke, F., Seth, I., and Whiteman, R. (2018, January 9). Bots, algorithms, and the future of the finance function. McKinsey.

- Research and Markets. (2021, April 19). Global Accounting Software Market (2021 to 2026) – Growth, Trends, COVID-19 Impact, and Forecasts. Research and Markets.

- Sage. (2020). The Practice of Now 2020: The essential report for accountants. Sage.

Leave a comment!