Cashless and contactless transactions have grown rapidly in the face of cybersecurity issues and health risks. Digital payment methods have given people the ability to be hands-free. Since digital transactions are so prevalent, your customers can also use their smartphones to make secure payments at any time of the day. The best mobile payments software does not even require the use of a standalone app, as wallets are integrated with messaging apps.

However, since there are countless mobile payment software on the market, it might be difficult to choose the best one for your business. This article will help you by shortlisting the best mobile payment solutions.

Best Mobile Payment Software in 2026 Table of Contents

Even before the pandemic, demand for companies that accept mobile payments had increased. In fact, the total value of the mobile payments market reached over $3 billion in 2019. The worldwide impact of COVID -19 was unprecedented, not to mention astonishing, as demand for mobile payment methods increased in all regions. The global market grew by 27.9% in 2020 compared to 2017-2019 and is expected to increase from $1.97 trillion in 2021 to $11.83 trillion in 2028, at an average growth rate of 29.1%.

Apple launched the mobile payment software, but other companies have followed suit. AliPay, PayPal, Amazon, and Mastercard are using AI to create new mobile payment options. With so many companies investing in mobile payment solutions, the average customer can pay using one’s phone, and there is no indication that this payment method will stop being preferred anytime soon.

Therefore, it makes sense for businesses to consider the trends in order to make informed decisions when implementing mobile payments software. Here are some of the trends to examine.

- Mobile Wallets. The year 2022 opens with 58% of mobile users reporting using a mobile wallet at least once a week, up from 46% in 2021. As customers get more familiar with mobile channels, they value their convenience and efficiency, leading to increased mobile wallet use. Digital channels make payments easier and reduce the risk of late or lost payments. Meanwhile, as Gen Z takes on increasing bill responsibility, billers must meet their expectations in the era of digital transformation. This would help attract and keep younger billpayers and convert older audiences to cost-effective, data-rich channels.

- Contactless Payments. More than half the global POS transactions will be contactless in five years, up from 15% this year. Contactless adoption in the United States will expand dramatically over the timeframe to 34% in 2022. Users’ unhappiness with chip card transaction speeds, along with growing contactless infrastructure, will boost the use of such payment methods.

- MPOS Technology. The global mPOS market is predicted to increase from $19.21 billion in 2019 to $62.46 billion by 2027, at a CAGR of 15.76%. In 2019, North America’s market was worth $7.68 billion, thanks to the region’s advanced technical infrastructure. Asia Pacific is expected to develop at the fastest rate at a 20.16% CAGR. Increasing India’s cashless economy effort will boost market growth in this region. Meanwhile, China’s mPOS business is growing rapidly as customers and retailers use it to buy everything from newspapers to drinks from vending machines.

- Social Shopping. Americans alone scroll for 5.4 hours per day, and smartphone users, in general, spend an average of 2 hours 24 minutes on social media globally. Merchants who meet shoppers on social media can make sound ways to encourage these shoppers to buy. Besides, consumers go to social media for their inquiries, to which merchants must respond fast. Over two-fifths of consumers expect social media answers within 60 minutes.

- Biometric Authentication. The value of remote mobile payments with biometric authentication is expected to reach $1.2 trillion by 2027. Biometric authentication is not limited to fingerprint and would also include facial recognition. However, some shoppers have been frustrated by facial recognition, despite its advanced technology and contribution to more secure transactions in payment gateways. Nevertheless, as technology improves and shoppers rely on fast and secure mobile payments, the use of biometrics is likely to continue.

- Flexible Payment Options. Shoppers want flexibility in how they pay and budget for mobile purchases. The buy now, pay later (BNPL) payment option gives shoppers ultimate payment flexibility. Given consumer familiarity, experts believe BNPL point-of-sale adoption will accelerate.

Source: Juniper Research

Best Mobile Payment Software in 2026

1. Apple Pay

Apple Pay is a secure way to pay for goods, services, subscriptions, and donations. In Safari apps and websites on iOS and watchOS, customers can authorize payments and provide contact and shipping information. iMessage and Business Chat extensions support Apple Pay. Touch ID, Face ID, and double-click on the Apple Watch help customers protect personal information.

Apple Pay stores users’ credit, debit, and bank account information, but will not share it with the recipient or merchant. This makes the transaction more secure, as digital criminals cannot interrupt it live. Apple Pay increases security and convenience for customers. It reduces wait times at payment counters and on one-touch purchases.

Detailed Apple Pay Review

By displaying the Apple Pay button on the shopping cart or product pages, you can offer express checkout. Simplifying transactions reduces purchase abandonment and increases conversion rates. Apple Pay works with Shopify, Salesforce, BigCommerce, WooCommerce, GoDaddy, Squarespace, Miva, IBM, Neto, Volusion, and Symphony Commerce. To drive mobile payments and repeat business, you can create contactless gift and reward cards.

Apple Pay is free to use for all Apple device owners. Accepting Apple Pay on websites, in iOS apps, and at point-of-sale terminals capable of contactless payments is also free for merchants. There’s no pricing plan for enterprises.

2. PayPal Here

PayPal Here is a free app for mobile and retail payments. PayPal’s own card readers can accept magnetic stripe, chip, and contactless payments like Apple Pay. PayPal Here lets you accept credit and debit cards from Visa, MasterCard, American Express, and Discover to a PayPal business account or a PayPal personal credit account.

You can expand with PayPal Here because the app is accessible anywhere with an internet connection. With its card readers, you can accept multiple payment types. In this way, you will never turn away a customer. Also, if you have offline payments enabled, you can process payments without an internet connection. However, offline payments will not be processed until the internet connection is restored and a request is made.

Detailed PayPal Here Review

PayPal Here can generate sales data, accept new users, create passwords and access levels, and manage inventory. For advanced features, you can integrate it with Vend, Lavu, and Touchpoint. In addition, linked PayPal Here devices can be used by approved enterprise users. Note that authorized people can use your PayPal account and the PayPal Here app.

You can download the PayPal Here app for free. Meanwhile, enterprise pricing for each transaction is quite manageable, and card readers are compatible with most iOS and Android devices for on-the-go or in-store payment processing. Prices for PayPal-owned card readers range from $14.99 to $79.99.

3. QuickBooks GoPayment

QuickBooks GoPayment is a mobile POS app for small businesses. You can combine it with QuickBooks Card Reader to accept payments with dip, swipe, and digital wallet. Using the GoPayment app in conjunction with QuickBooks Payments, your mobile business can accept payments without a third-party processor. The software is free for Android and iOS, but payment processing fees apply.

QuickBooks GoPayment can send invoices and make sure customers know what to pay. You can easily track whether notifications have been received and viewed. The system also syncs with QuickBooks Online and QuickBooks Desktop. This makes reconciling invoices and payments faster and less error-prone for merchants.

Detailed QuickBooks GoPayment Review

The QuickBooks GoPayment subscription does not automatically include a card reader. If you purchase a proprietary card reader, you can swipe the card. Otherwise, you can process payments through the solution’s iOS or Android app. You simply enter the transaction data and buyers authorize the card charge with a digital signature.

The vendor offers a free trial. QuickBooks Desktop Pay-as-you-go and QuickBooks Online Pay-as-you-go are free, while QuickBooks Desktop Pay costs $20.00 per month. Note that the chip and magnetic stripe card readers are sold separately. Businesses processing more than $7,500.00 per month can contact Intuit’s sales team for custom enterprise pricing.

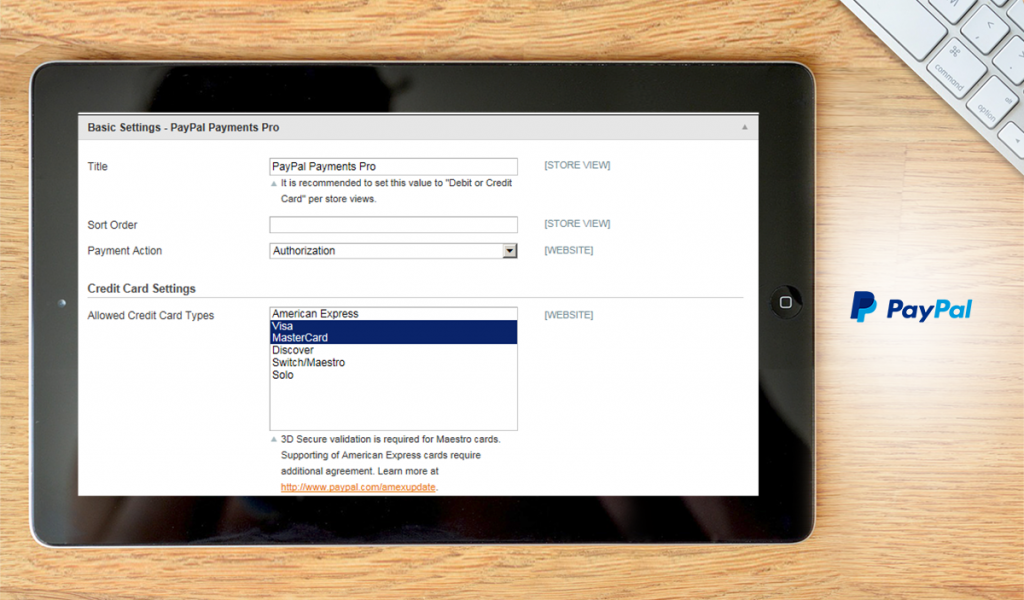

4. PayPal Payments Pro

PayPal Payments Pro is an enterprise-class ecommerce payment system that provides secure payment processing for the development of a professional ecommerce website. It can be customized to meet the needs of the business and is compatible with all devices. You can access more than 390 million active customer accounts worldwide.

The application is based on the techology of PayPal, one of the leading payment gateways. Paypal Payments Pro allows you to take credit card payments online and in stores. You can also develop and host your own checkout pages. Consumers pay 2.90%, plus $0.30 for each transaction, so your business benefits from large cards. The same apartment rate applies to debit, credit, corporate, and rewards cards.

Detailed PayPal Payments Pro Review

PayPal Payments Pro integrates with a variety of business systems and applications, including Shopify, 123 Contact Form, Wild Apricot, Formsite, and others. The app doesn’t require a PayPal account. However, it can accept online, phone, fax, and mail credit card payments (virtual terminal).

PayPal Payments Pro offers a simple pricing structure for its service, which includes APIs, easy shopping cart integration, online invoicing, and credit card payments by phone. It costs $30 per month with a flat fee for each transaction of 2.9% + $0.30.

5. Venmo

Venmo is a mobile payment service for Android and iOS. Consumers can share payments from their Venmo account, bank account, or debit card with family, friends, and approved businesses. Venmo balances, debit cards, bank accounts, and prepaid cards are free to use, but credit cards are charged 3%. Online and app purchases are free.

You can use Venmo to attract more customers by allowing them to share payments with friends. With this software, groups can share the cost of a single online or app purchase through the payment solution interface. At the same time, your business gets more exposure on social media conversations because Venmo also connects friends, family, and acquaintances. This increases your company’s chances of attracting new customers.

Detailed Venmo Review

To accept Venmo, you can integrate Braintree or PayPal Checkout. Venmo transactions are processed and settled similarly to normal credit card transactions.

Venmo is a free online and in-app payment service, and there are no pricing plans for enterprises. However, when integrating with Braintree and PayPal Checkout, Venmo payments incur the same fees as PayPal payments. Braintree fees are 2.9%, plus $0.30 per transaction, with custom pricing also available.

6. Square

Square is a POS that provides businesses with a reliable and fast system. It can be used at the counter or on the go with iOS or Android devices. The free software and Square magnetic stripe reader enable debit and credit card payments. The software also includes a real-time sales and inventory tracker and item management platform.

With Square, you can change the price, name, or quantity of an item in real-time. Employee passwords let you track who sold and refunded what. Meanwhile, customers can choose digital (email or SMS) or printed receipts. Open tickets and split receipts allow them to pay when it’s convenient for them, and split a bill by card or accept multiple payments. For advanced features, you can integrate Square with other business systems and apps like Vend, Weebly, and Wix, among many others.

Detailed Square Review

Square’s POS app and Magstripe Reader are free for iOS and Android. You can also purchase the Reader for Contactless and Chip, which charges the same amount for each insertion/insertion of major credit cards or smartphone tap (mobile payment) by your customer. You can upgrade to the Square for Retail monthly plan to get more sophisticated tools.

Note that Square is transaction-based, which means you will be charged a certain percentage for each tap, dip or swipe (credit card or mobile payment) on your POS device (tablet or smartphone with Square magnetic stripe reader or POS terminal with Square contactless reader).

7. Paya

Paya, formerly Sage Payment Solutions, enables online payments with credit and debit cards. This payment gateway offers online, virtual, POS, and mobile payments. You can accept cards, e-checks, and mobile wallet payments so you can accept payments from consumers with different preferences and never lose a deal. You decide what your business needs.

This software is PCI -, EMV-, and security-compliant. It protects every transaction from fraud with strict security measures and protects customer financial data and merchant reputation.

Detailed Sage Payment Solutions Review

Sage Payment Solutions connects with Sage accounting products to reconcile invoices and payments and synchronize front- and back-office activities. You can also set it up with ecommerce platforms like Shopify to make it easy for your customers to pay. Sage Payment Solutions also has APIs that allow developers to create custom connections with other applications.

The vendor does not offer a free trial. In the meantime, those interested should request a quote for their business.

8. Uphold

Uphold provides secure currency storage, exchange, and transactions. It allows companies to trade globally at a fraction of the cost. It is also transparent on fees. The fee structure is clear; there are no custody or maker-taker fees. Instead, Uphold charges spread fees, a tiny markup on the true market price.

Meanwhile, companies with distributed or global employees can use Uphold to pay fast compensation. Instead of remitting salaries through regular channels, companies can transmit them instantly.

Detailed Uphold Review

Uphold has an open API that allows companies and developers to create new applications on its platform. Most users have free access to the documentation, but companies that use the API for financial transactions must pay a regular fee of $0.35, plus 0.35% for each exchange.

Uphold does not charge fees for opening and holding funds, funding accounts, transferring and receiving money, or exchanging and buying currencies. However, in addition to third-party fees, Uphold charges fees for crypto withdrawals and bank transfers. Costs associated with exchanging real and digital currencies vary.

9. Dwolla

Dwolla facilitates internet bank transfers. It allows your business to accept ACH payments, an electronic payment method in the US, instead of cash, credit, debit, or check, so customers can send ACH payments to your business for credits and refunds. It is a flexible, easy-to-use product package that works with all US banks and credit unions.

With a verified business account with Dwolla, you can store funds received through payments in your account, similar to a digital wallet. You can use the funds in your account to make payments or transfer them to a business account.

Detailed Dwolla Review

Dwolla is also a popular API for transferring rewards and integrating P2P transfers into a user’s platform. It puts the brand first and provides the necessary payment infrastructure to ensure flawless payment processing.

Dwolla Pay-As-You-Go charges 0.5% per transfer. Enterprise rates start at $250 per month.

10. PaySimple

PaySimple automates small business receivables in the cloud. It offers a full suite of features and tools that reduce the time spent on tracking, sorting, and following up on payments so you can focus on what matters most. PaySimple’s expertise in recurring payments, including ACH and electronic checks, makes it ideal for businesses where transactions are repetitive, such as gyms.

The software does not come with its own card readers, POS terminals, or other hardware. However, card payments are still possible on-site. PaySimple’s app works on Android, iOS, and third-party mobile card readers.

Detailed PaySimple Review

PaySimple provides cloud-based software for accepting payments, billing customers, monitoring customer data, and setting up recurring payments. All of these features are fully customizable and requires no special skills. You can create invoices, submit them to customers and accept various payment types.

PaySimple integrates with QuickBooks Online, Jotform, WooCommerce, and ZenPlanner. Pricing plans start at $49.95 per month.

11. KakaoPay

KakaoPay is a PCI-DSS -compliant digital wallet that can be used with other Kakao services, including KakaoTalk. Businesses can pay bills and utility invoices online through the app or Kakao’s messaging service. The app also helps them to avoid missed or deferred bills and invoice payments to ensure smooth business operations.

PCI-DSS compliance protects your financial data. This digital wallet adds an extra layer of protection by requiring a password for each transaction. This reduces card theft and makes every user feel secure.

Detailed KakaoPay Review

With KakaoPay, you can offer scannable loyalty cards with barcodes. In this way, customers can collect rewards and points without losing them. This app is completely free and has no corporate plans.

12. Adyen

Adyen‘s mobile capabilities enable businesses to accept payments anywhere. It aims to replace credit card-PayPal combinations with one-touch mobile payment methods. Adyen focuses on debit and credit card purchases for the US ecommerce market and debit and Interact payments for Canada. The payment platform supports ACH, American Express, Diners Club, Discover, Mastercard, PayPal, Samsung Pay, and Visa.

Adyen supports the business environment by attracting more customers and making a product/service more accessible. Adyen enables online payments via local and mobile devices and guarantees that the money arrives on time, regardless of the buyer’s location.

Detailed Adyen Review

Adyen’s ability to connect with productivity tools and business applications is another reason it is a business-first payment technology. Adyen works with Salesforce, Ebizmarts, Navitaire, Cegid, Hybris, Magento, Amadeus, and others. Developers can create custom connections using plugins and open API data.

Adyen charges a calculated processing fee and commission per transaction. The payment method determines the fees and commissions. For example, Adyen’s pricing model for Visa, MasterCard, and other credit cards is based on interchange and scheme fees, as well as the acquirer markup.

13. Samsung Pay

Samsung Pay works with most store credit card terminals. In-app and online purchases can be made by loading cards into a digital wallet on a mobile device. This software typically requires no additional or upgraded equipment for business owners. It works almost anywhere customers swipe their credit cards without the need for an NFC terminal.

Samsung Pay works with NFC, EMV, and magnetic stripe readers, allowing stores to offer cashless payments. Customers spend less time at checkouts because they are processed quickly. It also works in Android apps and online stores.

Detailed Samsung Pay Review

Every Samsung Pay transaction is covered by the fraud protection of the credit card issuer or bank. PIN Transaction authentication must also be done via fingerprint or iris scan. Still, Samsung Pay adds extra layers of security with Samsung Knox and tokenization.

Samsung Pay does not charge users any additional fees for using the application. There are also no pricing plans for businesses.

14. Blockchain

Blockchain is a wallet for exchanging cryptocurrencies. You can use Bitcoin and Ethereum to trade securely and seamlessly with customers and other businesses. The app ensures that only authorized users can access the wallet, so a multi-level authentication mechanism and PIN protect the crypto wallet from intruders.

Blockchain helps you to find bitcoin merchants and service providers, makes bitcoin transactions easy, and separates their cash.

Detailed Blockchain Review

Like most wallets, Blockchain only charges for transactions, with fees calculated based on network conditions and transaction size. The priority fee is calculated to account for transactions within an hour. The regular fee is lower but it takes slightly longer than an hour for transactions to be confirmed.

Blockchain’s open API allows businesses to build unique connections. The Blockchain wallet is free and available in the app stores of Android and iOS devices. The web-based wallet works on all desktop operating systems.

15. SumUp Air

SumUp Air is a contactless EMV card reader. Your store can accept NFC, EMV, magnetic stripe, Apple Pay, and Android Pay with one device. Bluetooth connectivity makes it easy to manage payments. The device is powered by a lithium-ion battery that can last for hours and is charged via a micro USB port and plug.

Download SumUp to set up the card reader. Note that SumUp requires business, personal, and banking information. Then simply enter all your products into SumUp to streamline transactions. In this way you can print itemized statements. In quick sale mode, you can enter the transaction cost using the keyboard. The app will display the transaction after you press “Load.” Then your customers can pay contactless, by chip and pin or mobile.

Detailed SumUp Air Review

SumUp does not integrate with third-party receipt printers, so you have to send receipts to your customers via SMS or email. However, the SumUp 3G card reader with an integrated receipt printer is another alternative.

SumUp Air charges a one-time fee of $69.00 and 2.65% for each transaction. There are no pricing plans available to businesses.

16. MANGOPAY

MANGOPAY is a configurable end-to-end payment system for marketplaces, crowdfunding, and collaborative economic actors. It allows merchants and platforms to set up e-wallets for sellers, buyers, contributors, and project owners as well as collect payments and payouts automatically.

MANGOPAY’s white-label API allows businesses to create custom payment streams to optimize their business model with full security and flexibility in terms of users, e-wallets, and commissions. The app supports both domestic and foreign payment methods, making it ideal for global markets. Depending on the business model, MANGOPAY splits and deposits funds.

Detailed MANGOPAY Review

The payment management system secures payment data and transactions. It uses European KYC and anti-money laundering procedures.

MANGOPAY integrates with Katipult, Deemly, and ShareIn. You can even use it without the enterprise pricing plans or setup fees. There is only a transaction fee. In addition, volume discounts are available based on the total number of your monthly deposits.

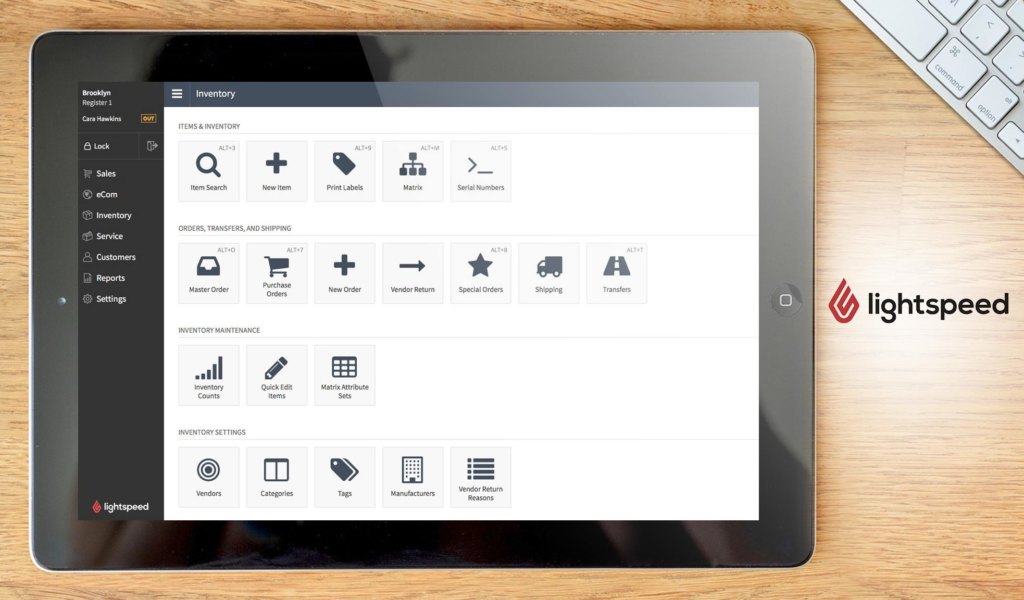

17. Lightspeed Retail

Lightspeed Retail enables businesses to accept in-store and online payments without third-party accounts. The software is PCI compliant, prevents global fraud, and encrypts data from start to finish. Fully integrated software allows business owners to retrieve batch reports and statements in real-time from POS. Lightspeed’s free dispute management and chargeback expert help businesses.

EMV-compatible terminals accept all major payment types at a low rate, regardless of the card network. Bluetooth-connected iPads can accept Mobile Tap payments. Available only in the US and Canada, Mobile Tap allows consumers to swipe their cards at the register, in the store, or at the curb. Mobile payments are convenient and reduce queues.

Detailed Lightspeed Retail Review

This top alternative to Apple Pay offers the ability to pay at multiple stores. This allows your employees to check inventory and sell from any store using an iPad. You can also assign serial numbers to your products. A matrix system allows you to vary the size, material, and color.

Lightspeed integrates with various business systems and applications, including Facebook, Agendrix, AppCard, and Bike Exchange, to name a few. The software is free to try, but rates range from $79 to $259 per month.

18. PhonePe

PhonePe is a UPI-based digital wallet used in the Indian subcontinent. Each online transaction requires only a single bank account or credit/debit card linked together. Regardless, the software protects customers’ financial data from criminals.

PhonePe is a useful software for your business as it allows your customers to pay their bills without missing anything or paying late. Also, they can use the software to pay staff. This feature will benefit your company with a global or dispersed workforce.

Detailed PhonePe Review

PhonePe stores can accept payments via POS, speeding up and simplifying in-store transactions. A POS is linked to a single retailer, ensuring security.

PhonePe charges a minimum transaction fee of ₹1 lakh. However, some software features, such as the ability to store money, are free.

19. Digipay.guru

Digipay.guru is a mobile payment platform for banks, merchants, retailers, fintech companies, and service providers. E-wallet solutions enable users to send and receive payments via QR codes, NFC-enabled devices, direct bank transfers, and unique IDs.

The app provides payment and recharge services. It allows users to reload digital TV and transit cards, top-up balances and cell phones, and pay postpaid bills, utility bills, and insurance. They can also provide international money transfer services for fast and secure cross-border money transfers.

Detailed Digipay.guru Review

The software helps merchants, retailers, and traders manage their business, make more money and offer frictionless payments. They can customize pre-made loyalty cards to engage customers. Digipay.guru helps them set up bitcoin wallets, manage all transactions, and get business data and reports.

Digipay.guru works with payment gateways, point-of-sale systems, virtual card providers, banks, MVOs, MVNOs, cryptocurrency networks, and beacon technologies. SME and enterprise pricing information for Digipay.guru is available upon request only.

20. TraQPayments

TraQPayments allows businesses to accept payments via QR, SMS, or email using multiple payment gateways. It handles multi-party settlements and manages processes easily. TraQPayments secures and tracks all purchases, from coffee to memberships. Your business can accept and settle multi-party payments automatically, even via mobile wallets.

They can add SMS billing, QR code scanning, and a mobile wallet to their service. This streamlines money collection with an intuitive interface and speeds up billing. Meanwhile, customers can pay with UPI QR, credit/debit cards, net banking, wallet, etc. You can find local businesses that accept TraQPayments.

Detailed TraQPayments Review

The software sends reminders and receives payment alerts so that customers with recurring payments receive a link on the selected day and time.

TraQPayments offers two subscription pricing options for businesses. Other fees include a 3% foreign credit card transaction fee.

Leverage Mobile Payment Software

Ecommerce and brick-and-mortar merchants need to keep up with payment trends in a rapidly changing digital world. Mobile payment methods offer convenience and a seamless shopping experience. If your store offers secure shopping and wireless payments, customers will come back.

That said, when deciding which software to use for your store, don’t just look at what offers the most features. Make sure the software you choose offers the features you need at the price that works best for you. Pay attention to integrations, scalability, and, of course, convenience for your customers.

Key Insights

- Apple Pay Dominance: Apple Pay stands out as the leading mobile payment software in 2024 due to its secure transactions, ease of use, and widespread acceptance across various platforms and devices.

- Growth of Mobile Payments: The global mobile payments market has seen significant growth, with a notable increase from $1.97 trillion in 2021 to a projected $11.83 trillion by 2028, driven by advancements in technology and changing consumer preferences.

- Diverse Options: Businesses have a plethora of mobile payment software options, each offering unique features tailored to different needs, such as PayPal Here for flexibility and QuickBooks GoPayment for integration with financial software.

- Security and Convenience: Security features like biometric authentication and encryption are crucial, as seen in solutions like Samsung Pay and Blockchain, which enhance customer trust and transaction safety.

- Trends in Mobile Payments: Key trends include the rise of mobile wallets, increased contactless payments, the adoption of mPOS technology, social shopping, and flexible payment options like buy now, pay later (BNPL).

- Integration and Customization: Many mobile payment solutions, such as Adyen and MANGOPAY, offer extensive integration capabilities with business systems and APIs, allowing for customized payment streams and improved operational efficiency.

FAQ

- What is the best mobile payment software in 2024? The best mobile payment software in 2024 is Apple Pay, known for its secure transactions, ease of use, and compatibility with various platforms and devices.

- How has the global mobile payments market grown in recent years? The global mobile payments market has grown significantly, increasing from $1.97 trillion in 2021 to a projected $11.83 trillion by 2028, with a 29.1% average growth rate, driven by advancements in technology and consumer demand for digital transactions.

- What are some key trends in mobile payments? Key trends include the rise of mobile wallets, increased adoption of contactless payments, the growth of mPOS technology, social shopping, biometric authentication, and flexible payment options like buy now, pay later (BNPL).

- What security features are important in mobile payment software? Important security features include biometric authentication, encryption, and multi-level authentication mechanisms, as seen in solutions like Samsung Pay and Blockchain, to ensure secure transactions and protect customer data.

- Why is integration capability important in mobile payment software? Integration capability is important because it allows businesses to connect their payment systems with other business applications and platforms, enhancing operational efficiency, customization, and overall customer experience. Solutions like Adyen and MANGOPAY excel in this area.

- What should businesses consider when choosing mobile payment software? Businesses should consider the features offered, pricing, integration capabilities, scalability, security, and convenience for customers when choosing mobile payment software. It is essential to select a solution that meets their specific needs and budget.

- How does Apple Pay enhance security for transactions? Apple Pay enhances security by storing users’ credit, debit, and bank account information securely and not sharing it with recipients or merchants. It also uses Touch ID, Face ID, and double-click on Apple Watch for authentication.

- What advantages do mobile wallets offer to customers? Mobile wallets offer customers convenience, efficiency, and security in transactions. They reduce the risk of late or lost payments and are increasingly popular among younger generations who value digital payment methods.

- How does mPOS technology benefit businesses? mPOS technology benefits businesses by enabling them to accept payments anywhere, increasing flexibility and convenience. The global mPOS market is expected to grow significantly, driven by the adoption of mobile payment solutions in regions like North America and Asia Pacific.

- What role does social shopping play in mobile payments? Social shopping plays a significant role by meeting consumers on social media platforms, encouraging purchases, and providing quick responses to inquiries. This integration helps merchants attract and retain customers in the digital age.

Leave a comment!