To start a business, the most crucial steps that you should tackle first are:

- Make sure you have a concrete business plan that details how you intend to get your ROI.

- Secure funding from reputable organizations.

- Ensure the legal and financial work are in order following local to federal regulations.

Being your own boss can be a liberating experience. This is why many individuals prefer owning a company than joining one. However, keep in mind that starting a business is as demanding as it is exciting. So, before you jump the gun, it might be wise to take a step back and first assess how exactly you’ll make it work. After all, how can you succeed in your entrepreneurial endeavors without first learning how to start a business?

In this article, we will be walking you through 12 easy steps of starting a business. We have detailed the process as best we can to help you plan for your success from finalizing your business idea to growing your company. We’ve also included some tips that you might find helpful as you set up your company. Hopefully, with this guide, you can make your journey towards entrepreneurship a little less daunting.

How to Start a Business Table of Contents

New businesses enter the market each day. In fact, according to the Kauffman Index Startup Activity, there are 550,000 new companies every month.

These entrepreneurs are setting up shop everywhere ranging from malls and office buildings to pop-up markets and online marketplaces. What’s more, they are determined to take consumers by storm with their novel ideas and passion for the industry. The only problem is that entrepreneurial spunk and resilience can only go so far. With that said, it comes as no surprise that many businesses fail before they make a profit.

The business employment dynamics data from the Bureau of Labor Statistics show that only 80% of businesses survive their first year. Even more alarming is that a mere 30% make it to their 10th year.

The sad part is that most of these businesses fail due to preventable issues. As you can see on the chart below, these issues include financing problems, incompetent team members, the lack of a business model, or poor marketing.

The Top Causes of Business Failure in 2018

Lack of market need: 42

Lack of market need

%Financing issues : 29

Financing issues

%Incompetent team: 23

Incompetent team

%Strong competitors: 19

Strong competitors

%Pricing/cost issues: 18

Pricing/cost issues

%Unhandy product: 17

Unhandy product

%Lack of business model: 17

Lack of business model

%Poor marketing : 14

Poor marketing

%Poor customer service : 14

Poor customer service

%Mistimed product : 13

Mistimed product

%Source: CB insights Research

Designed byThis just goes to show that planning will help you make your business endeavor last. It allows you to refine your ideas, understand your responsibilities as an entrepreneur, predict potential issues, and even gain insight into your target market. However, before you can do all this, you will first need to know how to start a business. So, without further ado, here is our step-by-step guide for new entrepreneurs.

The 12 Steps of Starting a Business

1. Fine-Tune Your Business Idea

So, you have a big business idea. Now what?

To move forward from ideation to execution, you have to start by refining your idea and the major details of your business. This is the time to be clear on what your business is going to be about. Try to get a better grasp of what your products or services aim to solve. Moreover, zero in on who your target audience is going to be. Now would also be the time to take a quick look at the current industry leaders. This way, you can find out how you can make your business better.

On the flip side, you might find yourself asking “what type of business should I start?” Well, if this is the case, you should probably take a break from reading this to go out and find inspiration. After all, the most original ideas come from your observations.

For instance, simply noticing that there’s no laundromat in your neighborhood can be a recipe for success. Perhaps, you could perfect a unique family recipe that’s been handed down to you and start a food truck business out of it. The point here is that the best small business to start is the one that your target market will need and one that you know you’ll be able to provide well.

2. Create a Solid Business Plan

Once you have a more concrete idea of what business you are going to put up, you’ll need to start laying the groundwork for your endeavor. This means drilling down the specifics of your business. In addition, you’ll need to know how to write a business plan so that you can write these down and organize them.

Some of the things that you’ll need to add to your business plan are:

- Business Name. It needs to be catchy and easy to remember so stay away from long names with hard-to-pronounce words. Also, be sure to check if it’s not being used by another company.

- Company Description. Describe what it is that your business offers as clearly as you can. The fewer the sentences, the better.

- Market Analysis. Conduct market research so you can study your competitors and survey your target market. Jot down and analyze your findings, making sure to justify why your business is needed.

- List of Products and Services. Enumerate all the products and services you aim to provide.

- Financial Statements. Prepare your income statement, cash flow projections, and balance sheets. These will help gauge the profitability of your chosen business.

In addition to these, you should also prepare documents detailing your business structure and funding plan. Your goal here is to simply map out how you intend to build and run your business. Remember, a business plan serves as your road map once you launch your company. With this at your disposal, you can easily visualize your endeavor, analyze your strategies, and prepare for potential obstacles.

3. Fund Your Business

Money is the lifeblood of businesses—no company will exist without working capital. Now the question is, how to start a business without money?

In this day and age, there are many ways to get funding so you can get your company up and running. You can try crowdfunding via sites like Kickstarter.com. This should help you find enough investors to execute your business idea. If that doesn’t work, you can ask for a little help from friends and family. In case this is not an option, you can try other financing options.

For instance, the most popular financing method is cash. This can be secured via bank loans, government-guaranteed loans, and grants. You should also try checking if you qualify for the loans offered by these organizations:

- Small Business Administration (SBA)

- U.S. Department of Agriculture (USDA)

- Small Business Innovation Research (SBIR) Program

- State and Local Business Assistance

- Small Business Lending Fund (SBLF)

- Small Business Investment Company (SBIC) Program

Just be sure to check out what kinds of funding plans they offer and what requirements they have. This will help you determine whether or not they can provide you with the backing that you need.

Source: Guidant Financial

4. Select Your Business Structure

Choosing a business structure is perhaps one of the most crucial decisions that entrepreneurs can make. It not only defines what type of company you have; it can also shape the way you perform your operations. This is because the type of business entity you select can pose long-term legal and tax consequences.

To help you get started, we have compiled some of the most common legal business structures of today. However, we highly recommend that you consult a qualified business attorney before making a decision. This way, you will know exactly what you are getting into.

- Sole Proprietorship. This is for businesses that are run and owned by a single person. However, this doesn’t separate your business assets from your personal assets. Meaning, entrepreneurs are personally liable for all business matters, including losses incurred due to debts and lawsuits. Moreover, they also need to handle all the invoices and transactions. Fortunately, they can rely on Zintego’s Invoice Templates for this purpose and streamline the work.

- Partnership. This is for companies with two or more owners. Like the previous structure, this creates no distinction between the entrepreneurs and the business entity. So, you won’t be shielded from any business-related losses.

- LLC. This is a common legal structure used by both US and non-US residents. It can be applied to companies with single or multiple owners. Moreover, it can protect your personal assets from any business-related debts.

- S-Corporation. This is a legal structure available only for US residents. With this, you can open up shares of your company to investors but allow you to avoid double taxation and self-employment tax.

- C-Corporation. This is for companies who not only expect to have investors but also want to go public in the future. The only problem with it is that the government can tax you twice–once when you file income taxes and another when you issue dividends to shareholders.

5. Register Your Business

Now that you’ve got your business details down to a T, you can register with the government to make things official. This includes filing your registration with the necessary local, state, and federal agencies.

To start, you will need to:

- File Your Business Type. As mentioned earlier, this is the legal structure of your business. You can do this by checking your state’s Secretary of State website. Just look for the business division.

- Get Employer Identification Number (EIN). This serves as your business’ tax ID number. You can get this from the Internal Revenue Service (IRS).

- Register for the Electronic Filing and Tax Payment System (EFTPS).This is required for payroll taxes. You can also get this from the IRS.

- Trademark Your Business Name and Branding. This one is optional but you should consider it if you want to protect your intellectual rights and make sure that no one else can use your name, logo, slogan, and branding. You can file this with the U.S> Patent and Trademark Office (USPTO).

6. Get Your Licenses and Permits

As a new entrepreneur, you have to start on the right foot. So, the next on our list of steps on how to start a business is to apply for licenses and permits.

You’ll need to get a federal permit if your business will involve activities that are regulated by a federal agency. These would include businesses that have anything to do with the following:

- Agriculture

- Fish and Wildlife

- Commercial Fisheries

- Alcoholic Beverages

- Aviation

- Maritime Transportation

- Mining and Drilling

- Nuclear Energy

- Firearms

- Radio and Broadcasting

- Logistics

As for local licenses and permits, these will depend on where you set up shop as well as the nature of your business. Different states, counties, and cities will require you to file for different permits. So, it is best to do your due diligence and take time to research them. In addition, you should clarify the validity of each license and permit so you can keep tabs on when to renew them.

7. Set Up a Mailing Address

We’ve heard it time and time again—email is king when it comes to business correspondence. So, why should you need a mailing address?

The simple answer is that most banks in the US will require you to provide a mailing address upon opening an account. It also makes your business appear more legitimate and professional to consumers. If this isn’t enough, listing your mailing address on your business website also makes you more searchable on Google, allowing you to expand your client reach.

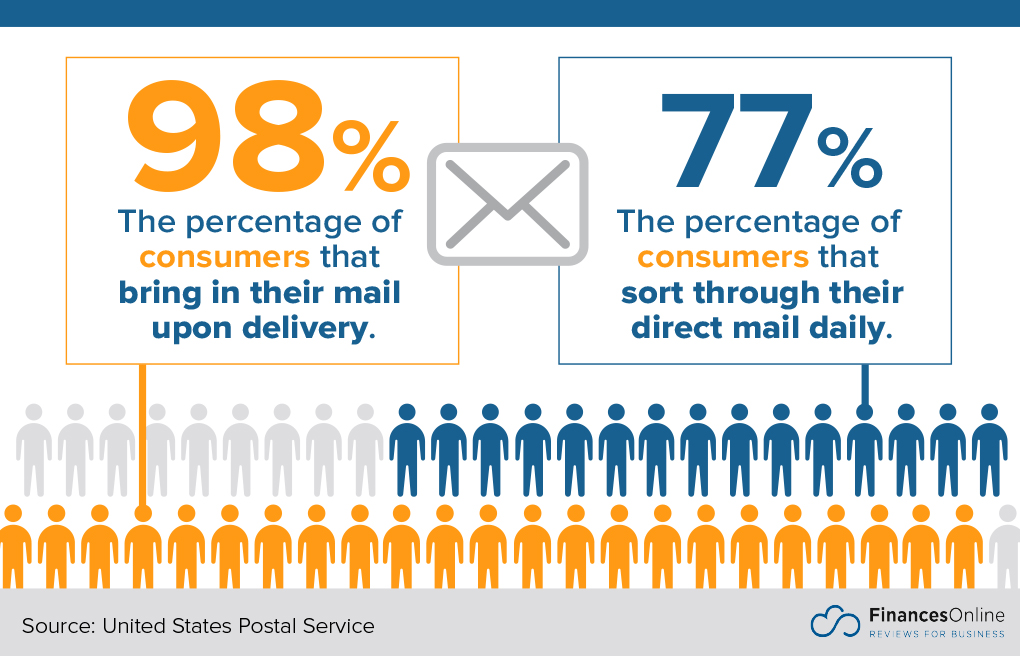

More importantly, there are other perks to having your own mailing address and using old-school direct mail for your company. For instance, email can end up in the spam folder where your intended recipients are never going to see it. Meanwhile, 77% of consumers still sort through their mail daily. This just means that there’s a higher chance that your potential clients will respond to you if you use direct mail.

8. Open a Bank Account

Every entrepreneur needs to be prepared once the money starts coming in. So, you will have to open a bank account for your business. Just be sure to take some of these factors into consideration before you finalize your banking details:

- Business bank account type. You can choose from a free business bank account, checking accounts, or savings accounts. If you aren’t sure, you can always consult your bank or your business attorney.

- Banking costs. No entrepreneur wants to hemorrhage money on banking fees. So, try to check if they offer competitive monthly service fees, ATM fees, and deposit fees.

- Online banking experience. As a busy business owner, you will need to manage your account from the comfort of your own home or office. So, make sure the bank offers a good digital platform where you can pay bills or make deposits.

- Convenience. Assess the location of the main bank and make sure that they have a network of branches and ATMs that will meet your requirements.

Of course, each bank will have a different set of requirements depending on the type of business structure you have so be sure to contact your prospective bank before you set an appointment. This way, you know exactly what documents to prepare and ensure a smooth application process.

In addition to a savings or checking account, you should also set up a merchant account for your business. This will allow you to accept payments from customers. Some of the most prominent providers in the industry are Stripe.com, Payoneer.com, Braintreepayments.com, Paypal.com. But in case you want more options, there are still plenty of other reliable payment gateways you can choose from.

9. Set Up Your Operations

You’ve ironed out the details of your business, got registered with the government, and secured all the permits needed to legitimize your company. So, now, you can begin setting up your operations.

A good place to start would be recruiting employees. To grow your business, you will need qualified individuals who are just as passionate as you are about your business. Try to look for those who possess strong work ethics, collaborative acumen, and technical competency. More importantly, find employees who are malleable and willing to learn more about the industry to improve your processes.

The next step would be to partner with reputable vendors, f.e if you are opening a bar business – you need order restaurant POS system. This one is a bit more tricky than employee recruitment. You will have to call for bids and closely evaluate submissions to make sure you will get your money’s worth. It would also make sense to monitor the vendor’s prior partnerships and performance to gauge whether or not they can meet your requirements.

Last but not least, we highly recommend finding software solutions to reinforce your operations. Statistics show that 73% of modern businesses plan on having fully SaaS-powered workplaces before 2020. To keep up, you should also look into automating aspects of your operations such as accounting, CRM, and marketing. Just be sure to assess them thoroughly.

If you aren’t sure which platforms you need, you should check out this list of SaaS tools for small business. This should give you a detailed explanation of the software solutions that new companies should have.

10. Get Insured

You never know when disaster will strike. What’s worse is, for small companies and startups, a natural calamity, property loss, or lawsuits can easily take a toll on their finances. This is why you will need to purchase insurance policies to protect your business from unforeseen circumstances.

Be sure to assess your risks early on in the business planning stage. After which, you need to find a licensed agent you can trust. Be sure to shop around for policies and not settle for the first policy that your agent shows you. This way, you can ensure you are getting the best coverage for the most competitive premiums.

Some of the most common types of insurance policies you should look into are:

- General liability insurance

- Product liability insurance

- Professional liability insurance

- Commercial property insurance

- Home-based business insurance

- Business owner’s policy

Additionally, the federal government requires all companies with employees to provide unemployment, workers’ compensation, and disability insurance. Some states also require additional types of insurance policies depending on the nature of your business.

11. Build Your Branding and Launch Your Business

The most crucial step to starting a business is launching it. After all, you can’t just open up your store and expect shoppers to come flocking to it right away. You’ll need to catch their attention well before your grand opening through strategic marketing.

To do this, you will first have to build your branding. Pick out a color scheme, font variations, and overall aesthetic that will embody the essence of your business. Make sure that this is consistent across your physical store, website, advertising materials, and promotional content. This allows you to build an identity for your businesses.

After which, you should formulate marketing campaigns to generate leads. Whether you are more interested in how to start an online business or a brick-and-mortar shop,

we highly suggest using a combination of different marketing strategies to yield the best results. Meaning, you should not only utilize advertisements but also leverage content publishing and even influencer marketing.

It is also important that you make your business visible on multiple channels. According to The Manifest’s 2019 Small Business Digital Marketing Survey, the top digital marketing strategies for startups include social media, websites, and email. So these should be good places for you to start.

In addition, you might want to make use of SaaS products to reinforce your marketing campaigns. Just be sure to study what is marketing software first as well as the types available on the market. This makes it easier to gauge which features you will require for your operations.

Top Digital Marketing Channels for Startups 2019

Source: The Manifest 2019 Small Business Digital Marketing Survey

Designed by12. Maintain Your Business

Last but not least on our steps to start a small business is maintaining your company. As you can see on this guide, starting a company is no walk in the park. It requires you to undergo lengthy legal processes, prepare countless documents, and spend quite a lot of money. So, don’t let your hard work go to waste.

Be sure to maintain your business not only by providing quality products and great customer service but also by remaining innovative. You should be prepared to adjust to any situation, making it a point to revisit your business plan every now and then. This allows you to adapt to consumer demands and market changes as quickly as possible.

In case you want to be more technical about your processes, you might also want to use a data-driven approach. There are plenty of business intelligence platforms for small businesses on the market that are easy-to-use but doesn’t skimp on functionalities. With these, you can check your KPIs and gain in-depth insight into your operations.

More importantly, you should also be a responsible company owner. This means you should also remain diligent in paying annual fees, filing your taxes, and renewing your permits. You need to do your best to remain up-to-date on city, county, and federal requirements. By doing so, you can make sure that all aspects of your operations are in order and avoid any problems later on.

Get Ready to Grow Your Business

Learning how to start your own business is only the first step to entrepreneurship. If you want your business to thrive, you will have to continue innovating in your chosen industry. So, expect to spend long hours and immense pressure to make your business work.

Remember, success does not happen overnight. To ensure that your business is on the right track, you should consider:

- Fostering strategic partnerships

- Proactively identifying new opportunities

- Investing in product development

- Providing personalized customer service

- Participating in events that are in line with your branding

By doing these, you can boost company reputation and expand the reach of your new business. Your small startup might even become a large corporation faster than you predicted.

If you are looking for other ways to further grow your business, be sure to check out our compilation of small business statistics. This should help you get an idea of the shifts in the business landscape so you can keep up no matter where your industry is headed.

Leave a comment!