With various financial challenges that have historically hounded the average African-American household, coupled with the result of the US fiscal cliff negotiations that set the stage for economic and social changes in 2013, some very important questions loom over the heads of many African-Americans. What does 2013 hold for them? If today’s hard work barely gets them through, what more do they need to do in 2013? Financial challenges seem to hit the hardest when the US economy is beset with an economic crisis. Can they afford more austerity, more debts and more sacrifices in 2013?

With various financial challenges that have historically hounded the average African-American household, coupled with the result of the US fiscal cliff negotiations that set the stage for economic and social changes in 2013, some very important questions loom over the heads of many African-Americans. What does 2013 hold for them? If today’s hard work barely gets them through, what more do they need to do in 2013? Financial challenges seem to hit the hardest when the US economy is beset with an economic crisis. Can they afford more austerity, more debts and more sacrifices in 2013?

Like the drastic worries brought by the US fiscal cliff talks, these are “draconian” questions that elude definite answers that will make sense to every African-American trying to make both ends meet at this very moment. What makes it even more difficult is the fact that there are differences in the way these challenges impact the lives of an African-American individual or household.

We may not have the best answers to these all too important questions, but we came up with an insightful list of the ten most pressing financial challenges that African-Americans will face in 2013. Aside from the perennial financial woes that badger African-American home and life, we came up with challenges brought about by changes in American taxation and government spending policies that we believe will prompt our readers to think “how can I better prepare myself and my family to meet these challenges?”

In the 2011 study The African-American Financial Experience conducted by the Prudential Group, the two main financial goals of an average African-American are increasing personal income and having some form of financial security in old age. The compelling motivation behind these goals is the desire not to be a financial burden to their families. Specifically, there are aspirations that are directly linked to the fulfillment of these financial goals. These are education, health, better jobs, higher income and business ownership. The items that make it on the list have profound impacts on these cherished financial goals.

What then are the ten tight and tricky financial challenges that will test the resilience of African-Americans in 2013? Here they are.

1. INADEQUATE MONEY

Lack of disposable income. Not enough emergency funds. Meager earnings. Call it what you want, the fact remains that inadequate money is still the top financial challenge facing the typical African-American household. Simply put, many African-American families will still struggle to pay for food, rent, gas and other necessities in 2013.

Based from the US Census Bureau’s 2011 Income, Poverty and Health Insurance Coverage report, poverty rate for African-Americans was up by 0.2 percent to 27.6 percent, or about 10 million living in poverty, out of the estimated 42 million African-Americans in the United States. Median income also dropped by 2.7 percent to $32,229, compared to the median household income of $50,054 for the rest of the US.

This is unlikely to change at all in 2013. The reasons are within the fast swirling cycle of income inequality. The other items in the list provide a clearer explanation in understanding and navigating this intricate and tricky web.

2. NO OR UNSTABLE INCOME SOURCE

Unemployment and underemployment still rank very high especially among US minorities like the African-American communities. The US Labor Department’s report for October 2012 revealed that unemployment rate for African-Americans rose almost a full point from 13.4 percent to 14.3 percent in September 2012.

Employment issue among African-Americans is deemed as a ‘structural” problem. With lesser opportunities for higher education and therefore better-paying jobs, African-Americans are more likely to get jobs in the public sector, where they are vulnerable to government job cuts in times of austerity measures. Data showed that some 600,000 government jobs have been cut in the 1st three quarters of 2012 alone, while 13,000 more were cut in October 2012. In the private sector, many African-Americans are first in line of downsizing, layoffs and last-in-first-out firing schemes, again citing marketable skills and job knowledge as major factors.

And with just a 12-month extension on jobless benefits as approved in the fiscal cliff negotiations , preparing for the inevitable – unemployment woes and lack of income source will definitely occupy the survival game plan of many African-Americans in 2013.

3. DEBT REPAYMENT

Plunging into debt becomes even more pronounced during times of economic crisis. The obvious reason is that during these times, it is the poor and low-income groups like African-Americans who are most likely to be affected in terms of cost-cutting measures like job reductions and reduced social welfare assistance. Money restraints, loan fixes and debt repayment constitute a cycle of debt load that will continue to confront many African-Americans in 2013.

Many areas in this article point to reasons why African-American households resort to debts and how they perpetuate the cycle of poverty. However, it is not only the low- and middle-income groups who are beset by debt repayment problems. Even middle class and affluent African-American households deal with reducing their accumulated debts.

The truth is, efforts by African-American individuals to break out from financial worries and improve income opportunities are actions that incur debts for them, albeit another tricky web. Student loans (in itself a separate financial challenge and discussed in the article as a separate item), home loans, medical debts and credit card debts are the top must-pay items.

Because African-Americans have been historically associated with disproportions in income-payment capacities, job instability and existing debts which are risk factors in home ownership, they are slapped with sub-prime loans of higher interest rates. And when the chance of home ownership eludes them, the typical African-American resorts to rents and leases. Worse, they incur more debts to manage rising rent and lease payments year after year.

When it comes to medical debts, the lack of adequate health coverage by most African-American households lead to major expenses once an emergency health situation besets them. Long-term prescription medications and treatments plus doctor’s fees and other costs are major expenditures that non-insured households are not prepared for, haven’t saved for and can only be paid by means of money proceeds from debts.

Meanwhile, the level of credit card debts is more serious than in seems. In the report Credit card statistics, industry facts, debt statistics by Creditcards.com, one in every three African-Americans own at least two credit cards, and that more than 90 percent of African-American families earning between $10,000 and $24,000 carry credit card debts.

4. STUDENT LOANS

Based from the 2011 report on student loan debt by the Federal Reserve Bank of New York, African-American students are most likely to graduate with huge debts, and they owe more than other students of different ethnicities.

The report showed that 85 percent of African-Americans who graduated in 2007-2008 have debts, compared to 47 percent of Hispanics, 40 percent of Asians and 72 percent of White Americans. African-American doctorate students owe an average of $68,000 while master program students own an average of $52,000 upon graduation. Interest rate hikes on major student loan sources such as the Stafford Loan, where African-American students are the single largest borrower group at five million (college, doctorate and master degrees) also makes matters worse.

Now, with almost three million African-Americans enrolled in college alone, both parents and students see student loan as the means to sustain college, and to pursue higher education. Payments would pile up if the college graduate chose not to work yet and go straight to MA or MBA, interest rates would increase steadily, and student loans remain a mainstay for 2013.

5. CREDIT WORTHINESS

Securing credit sources to start a financial goal rolling is another intricate and tricky web for African-Americans. Challenges that hounds the poor and the low wage earners such as unemployment, lack of savings and debt reports interplay with one’s credit worthiness.

Although lenders are prohibited by federal laws to discriminate against race when granting loans, studies still show a wide gap in credit scores between African-Americans and their white counterparts. In the study Credit Scores, Race and the Life Cycle of Credit conducted by the Federal Reserve System in 2008, data showed that the credit scores of African-Americans are consistently below their white counterparts and other racial groups in the US. Differences in age, income, neighborhood and marital status are some of the factors cited for the gap, factors where African-Americans are regularly at a disadvantage.

Establishing a good credit rating remains a dire situation for most African-Americans in 2013. With poor credit rating, it is next to impossible to get access to loans and credits for the more important things like improving the quality of life through better homes, education or having one’s own business.

And while resilience and determination can overcome this setback, it will take a great deal of sacrifice in terms of austerity to pay debts on time at least for a year to revive some level of credit eligibility. Serious savings can also be pulled off to be able to pay in full and thus, earn the right to request creditors to drop off delinquent credit ratings. With this, it seems the average African-American has his or her hands full in 2013 just dealing with credit worthiness alone.

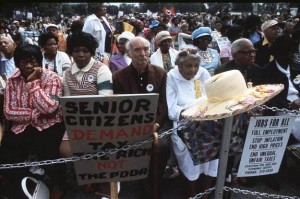

6. DOLE OUT FOR DEPENDENT FAMILY and RELATIVES

Helping fellowmen in need is a charitable deed that ranks high in the universal values of men, regardless of racial differences. It is a supreme act of kindness espoused by all religions of the world. However, helping out family members and relatives financially is never as strong or as pronounced as in the African-American community, nurtured by inherent faith-based values and done as society expects it from those with the means, no matter how small that may be, to help.

Helping fellowmen in need is a charitable deed that ranks high in the universal values of men, regardless of racial differences. It is a supreme act of kindness espoused by all religions of the world. However, helping out family members and relatives financially is never as strong or as pronounced as in the African-American community, nurtured by inherent faith-based values and done as society expects it from those with the means, no matter how small that may be, to help.

A 2011 survey by The Washington Post-Kaiser Family Foundation covering 800 African-American women revealed that almost half of them help out relatives, while over one-third gives financial assistance to family members and even friends. Child care and elderly needs are top reasons for the dole-out. Indeed, many African-American adults still get financial aid from their parents and other family members for child care to mortgage payments.

Despite the fact that African-American women are not financially stable themselves, they remain as important source of doled-out financial assistance to dependent family members and relatives.

The report More Black Women Going Bankrupt by Black Enterprise says that in the months leading up to the fiscal cliff peak, many African-American women are drawing out emergency funds from their retirement savings for emergency expenses. More and more African-American women are filing for bankruptcy or defaulting on their loans, while loan sharks are on standby to prey on those who do not have access to traditional loans or have been cut out due to failing credit worthiness.

Indeed, many African-American women are the stronghold of their households and families, but “until when?” is the big question. With higher taxes and more difficult access to financial sources , the typical African-American breadwinner may need to sustain first his or her needs, and we all know this is a sad development both for the dependent and the breadwinner.

“RENEWED” CHALLENGES

While every American is likely to be affected by recent developments in US taxation in 2013, many sectors warn that when it comes to the final US fiscal cliff measures, the low and moderate income earners would be hit the hardest. Needless to say, these would be African-Americans and other US minorities.

While the few agreements reached in the Senate and approved by Congress (such as the extension of the unemployment benefits for only a year and the extension of the college tuition tax credits for five years)are welcomed by low and middle-class wage earners, it is important to note that some welfare benefits like unemployment assistance is only good for a year. More importantly, negotiation on domestic (and defense) program spending cuts has been halted. Needless to say, uncertainties still loom.

7. MORE TAX PAYMENTS

In the last minute negotiation, the US Congress passed an agreement increasing taxes for married couples with over $450,000 income and individuals with over $400,000 from 35 percent to 39.6 percent. Americans on this income bracket will also deal with higher taxes for their dividends and capital gains from 15 percent to 20 percent. Couples earning more than $250,000 and individuals filing over $200,000 in income were still not spared, as the limits on personal exemptions and itemized deductions for them were also passed.

In the last minute negotiation, the US Congress passed an agreement increasing taxes for married couples with over $450,000 income and individuals with over $400,000 from 35 percent to 39.6 percent. Americans on this income bracket will also deal with higher taxes for their dividends and capital gains from 15 percent to 20 percent. Couples earning more than $250,000 and individuals filing over $200,000 in income were still not spared, as the limits on personal exemptions and itemized deductions for them were also passed.

For the rest of the working Americans, a 2 percent payroll tax increase for all wage earners is the verdict.

As emphasized, automatic cuts in federal spending on domestic programs (along with defense) remain to be addressed. With no clear compromise on the horizon, this will derail any financial goal and plan that most African-American households earning $32,000 to $50,000 annually (the median household income for this group as of 2011) have started. For those even below the poverty threshold, effects on domestic programs they depend on can be a matter of literally surviving a day.

8. FUNDING BASIC EDUCATION

Access to good quality education has always been a perennial challenge hounding the young African-American and their parents, and this continues after 2012. While the tax credit for college tuition was extended in the fiscal cliff agreement for five years, giving temporary relief to some 25 million low income families, what lies ahead in terms of non- tax-related changes remains something to be prepared for.

Access to good quality education has always been a perennial challenge hounding the young African-American and their parents, and this continues after 2012. While the tax credit for college tuition was extended in the fiscal cliff agreement for five years, giving temporary relief to some 25 million low income families, what lies ahead in terms of non- tax-related changes remains something to be prepared for.

African-American leaders have been vocal about concerns on spending cuts in education, as these would be most damaging to their children and young adults. NPR National Correspondent Corey Dade in his article Blacks, Latinos Join White House In ‘Fiscal Cliff’ PR War said that spending cuts in education would be among the most detrimental to their (African-American) communities. “Vulnerable programs include student loan subsidies and Pell Grants for college students, and Title 1 funds for public schools with high enrollments of students from low-income families. Roughly 50 percent of America’s public schools receive Title 1 money,” he said.

In some cases, apart from insufficient funding in schools, the internal educational structure which is assailed by so many issues – program, curriculum, leadership and student body, also serves as a barrier for young African-Americans to sustain their journey to education.

9. PAYMENT FOR HEALTH INSURANCE

The US Supreme Court upheld President Obama’s Health Care Law, requiring all Americans to be covered by health insurance. While the law has many benefits to its credit as far as reforms in US health plans and insurance malpractices are concerned, the clause on mandatory coverage, and how the average African-American will pay for it, cannot be ignored as a legitimate cause for worry in 2013.

For affluent taxpayers, there’s the grievance of paying the extra tax money to make this law happen, a burden reduced to nothing compared to thousands of African-American families with no stable employment and thus no employer-sponsor counterpart to depend on for premium payments.

For households with very low Medicare coverage, getting a supplemental health insurance is necessary, something they have to save and spend for. For this group struggling to make both ends meet on a daily basis, it’s where to get the money to pay for their health insurance. An Associated Press report, Partial list of taxes and fees in health overhaul said that non-coverage means penalty payments of about $1,200 starting in 2014.

10. FUNDING SMALL BUSINESS

In a white paper titled Financial Obstacles Faced by African American Entrepreneurs: An Insight into a Developing Area of the U.S. Economy published in the Journal of Developing Areas by the Tennessee State University, the financial challenges faced by African-Americans wanting to become entrepreneurs come from four capital-related dimensions: outside funding, insurance costs, cash flows and internal financial management. These boil down to lack of capital as the main reason preventing them from starting this life-changing plan. Would-be African-American entrepreneurs are also hindered by lack of basic business knowledge, trying to saving for more urgent areas in life and day-to-day money issues.

In a white paper titled Financial Obstacles Faced by African American Entrepreneurs: An Insight into a Developing Area of the U.S. Economy published in the Journal of Developing Areas by the Tennessee State University, the financial challenges faced by African-Americans wanting to become entrepreneurs come from four capital-related dimensions: outside funding, insurance costs, cash flows and internal financial management. These boil down to lack of capital as the main reason preventing them from starting this life-changing plan. Would-be African-American entrepreneurs are also hindered by lack of basic business knowledge, trying to saving for more urgent areas in life and day-to-day money issues.

Two business-related tax policies are meant to encourage those with the dream of putting up their own business, but complicated terms seem to make the dream harder to realize. For instance, the Earned Income Tax credit (deductions for running one’s own business) comes with stringent eligibility terms on income limits, maximum credit and updates on US tax laws.

And while the Small Business Jobs Act of 2010 was meant to help small businesses, some terms were seen to benefit the big investors (like the 100 percent exemption of taxes on capital gains) and holders of shares of stocks while encouraging loan availments of would-be entrepreneurs. The average African-American wanting to start a small business still must find a more solid and “affordable” means of funding assistance to move on from being daily wage workers to self-employed or employers.

PROPOSED SOLUTIONS and CALLS TO ACTION

Indeed, some of these financial concerns have been chronic presence in the everyday life of African-Americans and linked to issues as far back as the Civil Rights Movement and African-American economic disenfranchisement. Hence, one wonders why, despite principal changes meant to better the lives of African-Americans, their economic condition remains slow-moving, if not stagnant and embroiled in a cycle of poverty.

Adding salt to wounds, recent increase in tax payments and inevitable changes on jobs, education and on domestic program funding as a whole will surely affect many African-American households. What to do?

First, start with the “self.”

Learn the ropes of personal financial management. Understandably, those who have just enough to get on with the day don’t have the means to pay for professional finance advisors. It’s not a problem. You can learn on your own. Use free resources available for you like library books and magazines and personal finance websites.

Talk to people in your community whom you can trust to have a good knowledge on money management – professors, community counsellors, your church leaders and your co-workers. Even your business woman-neighbor may have a thing or two to teach you about managing your personal and household money.

Better yet, learn with your spouse and your kids. Understand and learn how to solve money problems as a family. As the saying goes, there is strength in numbers, and even the most challenging financial situation is no match against the collective dedication and willpower of one determined family. Practice what you learn and apply them in your everyday life.

Second, get your acts together.

African-Americans should get involved, passionately, where their future is concerned. Take active part in legislation and ensure that these measures truly consider African-American perspectives. Justice and equality cannot be achieved by mere silence, indifference and passivity especially when the lives of millions of people and their future are at stake, with long-term effects to personal lives.

African-Americans should get involved, passionately, where their future is concerned. Take active part in legislation and ensure that these measures truly consider African-American perspectives. Justice and equality cannot be achieved by mere silence, indifference and passivity especially when the lives of millions of people and their future are at stake, with long-term effects to personal lives.

Advocate and demand for legislation that will materially bring a change in terms of unbuckling economic chains that bound the average African-American to the cycle of poverty and inequality in opportunities.

Third, focus.

Education is a key area in this change, and being a point of focus in the shared financial goals of African-Americans which we have highlighted, it is one area where what needs to be done must not be delayed or worse abandoned in the face of challenges. With education comes equal opportunities in jobs, salaries, financial access and chances in being economic players, moving from being paid employees to employers themselves.

Fourth, keep the faith and the inspiration.

Another important thing is for African-Americans, like any other racial groups in the world, to accept some of their flaws as a group and resolve to correct them. Positive change is a two-way process. Wallowing in obsolete and negative notions, such as African-Americans being mere helpless “victims” of circumstances, do nothing to uphold the sense of greatness as showcased in the deeds of the likes of Martin Luther King Jr., Frederick Douglass, Mary McLeod Bethune, Linda Brown and other great African-American leaders and inspirations.

Fifth, act and do what needs to be done.

Despite many challenges, much has changed and improved in the lives of men today. Think of African-American leaders and forefathers who have valiantly broken down walls of inequality and fought suppression, how much more great things they could have done with the opportunities and chances today. The doors have been opened and the paths cleared by them. It’s up for every African-American to value the sacrifices of their forefathers and do something to ensure that the true meaning of equality and justice is never lost in their generation.

To put it plainly: Speak up. Get up. Move on. Study. Work. Help. Aspire. Achieve. Succeed. Look back and succeed even more. The year 2013 with all its challenges and surprises is the perfect time to begin.

EXCELLENT information! Not everyone (black) is in debt, but some are hopefully we can get out fast! THANK YOU!

Leave a comment!