In today’s digital economy, businesses rely on online payment gateways to process transactions securely and efficiently. Whether you run an eCommerce store, a SaaS business, or a subscription-based service, choosing the right payment gateway is crucial for minimizing costs and maximizing profits. However, understanding payment gateway fees can be complex due to the different pricing models, transaction charges, and hidden costs involved.

This guide provides a comprehensive breakdown of payment gateway fees, covering various pricing structures, cost components, and factors influencing transaction charges. By the end, you’ll have a clear understanding of how payment gateway fees work and how to choose the most cost-effective solution for your business.

What is a Payment Gateway?

A payment gateway is a technology that securely facilitates online transactions by acting as a bridge between a merchant’s website or application and financial institutions such as banks and credit card networks. It is not just a transaction processor; it serves as a crucial security platform for business, protecting both merchants and customers from fraud and unauthorized access to payment data. By encrypting sensitive payment data, verifying transactions, and managing authorization requests, a payment gateway ensures that funds are transferred safely from customers to businesses.

How Payment Gateways Work

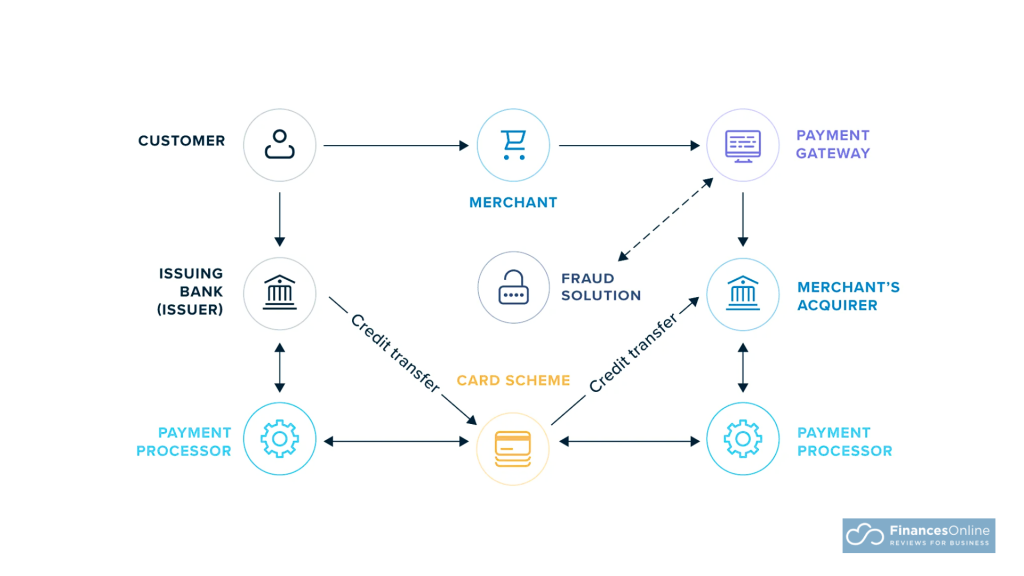

A payment gateway facilitates the secure transfer of funds between customers, merchants, banks, and payment processors during an online transaction. The process involves multiple entities working together to ensure smooth and secure payments.

- Customer Initiates Payment – The customer selects a product or service and enters payment details, such as a credit/debit card or digital wallet.

- Payment Gateway & Merchant’s Acquirer – The payment gateway encrypts the payment details and forwards the transaction request to the merchant’s acquiring bank, which then communicates with the payment processor.

- Transaction Authorization – The payment processor routes the request through the card scheme (Visa, Mastercard, etc.) to the issuing bank, which verifies the customer’s funds and either approves or declines the transaction.

- Fraud & Security Check – Fraud prevention systems analyze the transaction for risks before approval.

- Funds Settlement – If approved, funds move from the issuing bank through the card scheme to the merchant’s acquirer, then to the merchant’s account, usually within 1-3 business days.

This process ensures fast, secure, and efficient online transactions.

“A secure payment gateway is not just about processing payments; it’s about ensuring trust between businesses and customers. Choosing a gateway with strong encryption and fraud protection is critical in today’s digital landscape,” — Arvind Rongala, CEO of Edstellar.

Types of Payment Gateway Fees

Payment gateways charge merchants different types of fees based on transaction type, business model, and pricing plan. Among these, transaction fees are the most significant cost factor, directly impacting a business’s profitability.

1. Transaction Fees

Transaction fees are the most significant cost component and are charged per successful transaction. They usually consist of two components:

- Fixed Fee: A predetermined amount charged for every transaction, such as $0.30 per payment.

- Variable Fee: A percentage-based fee applied to the total transaction amount, typically around 2.9% per sale.

For example, if a payment gateway charges 2.9% + $0.30 per transaction, a $100 sale would incur a fee of:

(2.9% of $100) + $0.30 = $2.90 + $0.30 = $3.20.

Businesses with high transaction volumes should compare payment processor fees to minimize costs. Optimizing for low transaction fees and negotiating customized pricing can help maximize profits while ensuring seamless payment processing.

“Businesses often overlook the impact of small transaction fees on their bottom line. A 0.5% difference may not seem like much, but for high-volume merchants, it could mean thousands of dollars in extra costs annually,” — Jacob Hale, Lead Acquisitions Specialist at OKC Property Buyers.

2. Monthly Fees

Some payment gateways charge a fixed monthly subscription fee to access their platform and additional services. These fees often cover:

- Fraud Protection – Advanced security measures to prevent fraudulent transactions.

- Customer Support – Dedicated assistance for payment-related issues.

- Premium Features – Advanced reporting, recurring billing, or multi-currency processing.

Examples of monthly fees:

- PayPal Pro – $30/month

- Authorize.Net – $25/month

3. Setup Fees

Some enterprise-level payment gateways require a one-time setup fee for account activation and integration. This fee is common among providers offering custom payment solutions tailored to specific industries. While many modern payment gateways (like Stripe and Square) do not charge setup fees, others may impose costs ranging from $50 to $500 depending on the provider.

4. Refund & Chargeback Fees

- Refund Fees: Some gateways charge a processing fee when a merchant issues a refund. While some providers return the transaction fee, others retain a portion of it.

- Chargeback Fees: If a customer disputes a transaction and wins the claim, the merchant is hit with a chargeback fee, typically $15 to $50 per dispute.

“Chargeback fees can eat into profits fast. Businesses should focus on proactive fraud prevention and clear refund policies to avoid unnecessary disputes.” — Matthew Holland, Head of Marketing at WellPCB.

5. Cross-Border Fees

Merchants processing international transactions often face cross-border fees due to currency conversion and foreign banking regulations. These additional charges typically include:

- Currency Conversion Fees – Ranges from 1% to 3%, depending on the exchange rate and the payment processor.

- Cross-Border Transaction Fees – Payment gateways may add an extra 1% or more for transactions processed outside the merchant’s home country.

💡 Tip: Businesses with frequent international transactions should consider local payment processors or multi-currency merchant accounts to reduce costs.

6. PCI Compliance Fees

The PCI DSS checklist requires businesses to protect customer payment data. Some payment gateways charge an annual PCI compliance fee, typically ranging from $100 to $200, to cover security maintenance and compliance checks.

💡 Tip: Choose a PCI-compliant gateway that includes security features in its pricing to avoid separate compliance charges.

7. Settlement & Withdrawal Fees

Merchants may incur additional fees when withdrawing funds from their payment gateway to their bank account. These include:

- Standard Bank Transfer Fees – Some gateways charge a small fee for fund withdrawals.

- Instant Withdrawal Fees – For faster access to funds, businesses may pay 1% or more (e.g., PayPal charges 1% for instant transfers).

How to Minimize Payment Gateway Fees

Payment gateway fees can add up quickly, significantly impacting a business’s profitability. However, by adopting strategic cost-saving measures, businesses can reduce transaction costs, optimize payment processing, and increase their bottom line. Below are some key ways to minimize payment gateway fees while maintaining a seamless customer experience.

1. Choose the Right Pricing Model

Not all pricing models are suited for every business. Selecting the best structure based on transaction volume can help reduce costs:

- Flat-rate pricing (e.g., 2.9% + $0.30 per transaction) is ideal for small businesses with low transaction volumes.

- Interchange-Plus Pricing offers transparent rates and can be cheaper for high-volume businesses since merchants only pay the interchange fee plus a small markup.

- Subscription-based pricing (e.g., $99/month + $0.05 per transaction) is beneficial for merchants with high monthly sales, as it reduces per-transaction costs.

2. Reduce Chargebacks

Chargebacks not only result in lost revenue but also incur additional fees ranging from $15 to $50 per dispute. To minimize chargebacks, businesses should:

- Use fraud detection tools to identify suspicious transactions.

- Display return and refund policies to set customer expectations.

- Provide 24/7 customer support to resolve issues before disputes escalate.

- Utilize address verification (AVS) and CVV matching for added security.

💡 Tip: Preventing chargebacks through fraud prevention and clear policies is cheaper than dealing with disputes.

3. Encourage Alternative Payment Methods

Credit card transactions typically come with high processing fees. To lower costs, businesses can:

- Encourage ACH bank transfers, which have lower transaction fees (as low as 0.5% vs. 2.9% for credit cards).

- Offer digital wallets (Apple Pay, Google Pay, PayPal), as some may have reduced fees compared to direct card payments.

- Accept Buy Now, Pay Later (BNPL) services, which may offer lower merchant processing fees than traditional credit cards.

💡 Tip: Offering diverse payment options improves customer satisfaction while reducing processing costs.

4. Negotiate with Payment Processors

Many merchants assume that payment gateway fees are fixed, but they can often be negotiated, especially for high-volume businesses. Steps to secure better rates include:

- Contacting multiple payment providers and comparing rates before signing a contract.

- Asking for lower transaction fees if processing large volumes.

- Inquiring about custom pricing models tailored to your business needs.

“Many businesses assume payment gateway fees are fixed, but that’s not true. If you process high volumes, you should always negotiate rates—it can save you significant money over time,” — Gary Hemming, Owner & Finance Director at ABC Finance.

5. Optimize Settlement Periods

Optimizing settlement periods is a simple yet effective way to reduce payment gateway fees. A settlement period refers to the time it takes for funds from a transaction to be deposited into a merchant’s bank account. Many payment processors offer instant withdrawals, but these come with high transaction fees, typically 1% or more per transfer (e.g., PayPal charges 1% for instant bank transfers).

To lower payment processing costs, businesses should:

- Opt for standard settlement periods (typically 1-3 business days) to avoid extra charges.

- Plan cash flow effectively so they don’t have to rely on expensive instant withdrawals.

- Choose payment gateways with lower withdrawal fees for cost savings.

6. Use Local Payment Gateways for International Transactions

If your business processes international transactions, you might be paying high cross-border fees and currency conversion charges. Using a local payment gateway can significantly reduce foreign transaction fees and improve customer trust and conversion rates.

Key benefits of local payment gateways:

- Lower cross-border transaction fees (often saving 1% or more per transaction).

- Better currency conversion rates than international payment processors.

- Increased customer confidence by offering familiar, region-specific payment options.

Popular local payment processors include:

- Alipay (China)

- PayU (India, Latin America)

- Klarna (Europe)

“For global businesses, partnering with region-specific payment providers can significantly lower fees. Localizing payments is an overlooked strategy that can improve both costs and customer conversion rates,” — Gil Dodson, Owner of Corridor Recycling.

Conclusion

Understanding payment gateway fees is essential for optimizing costs and maximizing profitability. Businesses must evaluate different pricing models—flat-rate, interchange-plus, or tiered pricing—to select the most cost-effective option. Reducing unnecessary transaction fees, avoiding hidden charges, and minimizing chargeback fees can lead to significant savings. Additionally, negotiating better rates with payment processors—especially for high-volume transactions—can further cut costs.

When choosing a payment gateway, consider transaction costs, monthly subscription fees, cross-border charges, and payout schedules. Some providers offer volume discounts or lower fees for specific payment methods, so comparing multiple options is key to saving money.

By selecting the right payment processing solution and optimizing fee structures, businesses can improve cash flow, enhance checkout experiences, and increase revenue. A well-optimized online payment system not only reduces expenses but also improves customer satisfaction, leading to higher conversions and long-term business growth.

Leave a comment!