How to Commit to a Life Savings Goals: Checking Your Money Views

This article is Part 3 of 5 of

Your Total Guide to Managing Life Savings: Exposing The Best-Kept Secrets

Money problems and issues can be better resolved by informed decision-making, and this can only be done when one is equipped with the knowledge and skills in managing life savings.

Money problems and issues can be better resolved by informed decision-making, and this can only be done when one is equipped with the knowledge and skills in managing life savings.

Here’s a guide on how to manage your life savings so that it continues to grow and you remain focused on rebuilding it even if there are things that come up that sidetrack your original savings goals.

Determine what will drive you to maintain and stick to a life savings account

Probably more important than how much your money is, your mindset about your life savings will spell the difference between simply having a saved amount of money today and actually looking forward to a comfortable future.

If you have vague ideas of why you are putting up a life savings fund when you already have your standard savings account or two and an emergency fund, then it will be easy for you to get sidetracked both in faithfully adding up to your life savings account and in using it for a different purpose.

Once you know the raison d’etre – the compelling reasons why you need to build a life savings, you will be more committed to build and maintain that one major life fund as you look ahead into the future with all your important life goals organized and accomplished.

Know the sources of funds for your life savings

If you have recognized the value of having a life savings and what it is for, the next important step is to know how you will grow it. So what goes into your life savings? For those who have more than one income, having a mix of money sources from which to get “contributions” for your life savings fund is a good way to ensure your money grows consistently.

Incomes need not be from jobs or business profits alone, as cash gifts, incentives from special projects you’ve done and cash rewards you may receive from ordinary spending activities may be funding sources for your life savings account too.

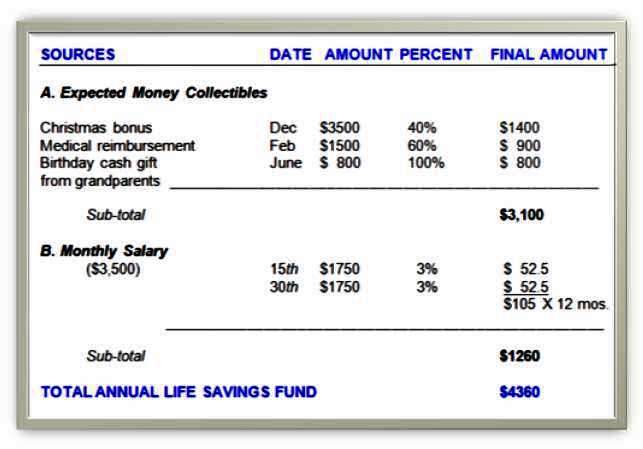

SIMPLE LIFE SAVINGS PLAN SHOWING VARIOUS SOURCES AND PERCENTAGE

In the simple fund sourcing plan above, the annual life savings fund to be earned from two major sources (annual money collectibles and monthly salary) amounts to $4,360 a year, or simply $87,200 in 20 years. (Of course, our simple example does not include the eventual annual increase in deposits over the years as the expected collectibles and salary will also go up.)

By knowing the sources of major funds for your life savings, making earnings and timeline projections will be easier and your goal accomplishments doable and within reach.

Create an “infusion” schedule and stick to it

The schedule for injecting money into your life savings need not be a strict regular routine, especially if you are also maintaining standard savings account and an emergency fund. It is common for the usual payroll extra especially for those with budgeted expenses and fixed savings to allot this to the standard savings. Which is alright and sensible.

The schedule for injecting money into your life savings need not be a strict regular routine, especially if you are also maintaining standard savings account and an emergency fund. It is common for the usual payroll extra especially for those with budgeted expenses and fixed savings to allot this to the standard savings. Which is alright and sensible.

Because of the nature of the life savings fund (financial preparation for big-ticket items or major life events), these things take time and planning. In the same way, your life savings meant to accomplish these goals can also take the same pace. Gradual, yet big. A schedule for adding up into your life savings could coincide with an expected money collectibles within the year, like profit sharing or bonuses at work, cash tax reimbursements, earnings from some investments you made, and similar “collectibles.” If you want to include a portion of your monthly earnings too as a personal choice, well and good.

The emphasis in keeping a schedule is for you to stick to maintaining your life savings fund, and erasing any conflicts where your standard savings and emergency fund comes in. It also makes building and growing your life savings less of a pressure, knowing that you have money coming in to look forward to that would have a definite purpose on how you will use it. Just make sure you stick to it.

Do you know the answers to the three most common questions asked during money emergencies?

Continue reading Part 4: How To Deal With Money Emergencies

Leave a comment!